Cyclopedia

of

Commerce, Accountancy,

Business Administration

Volume 1

A General Reference Work on

ACCOUNTING, AUDITING, BOOKKEEPING, COMMERCIAL LAW, BUSINESS

MANAGEMENT, ADMINISTRATIVE AND INDUSTRIAL ORGANIZATION,

BANKING, ADVERTISING, SELLING, OFFICE AND FACTORY

RECORDS, COST KEEPING, SYSTEMATIZING, ETC.

Prepared by a Corps of

AUDITORS, ACCOUNTANTS, ATTORNEYS, AND SPECIALISTS IN BUSINESS METHODS AND MANAGEMENT

Illustrated with Over Two Thousand Engravings

TEN VOLUMES

CHICAGO

AMERICAN TECHNICAL SOCIETY

1910

Copyright, 1909

BY

AMERICAN SCHOOL OF CORRESPONDENCE

Copyright, 1909

BY

AMERICAN TECHNICAL SOCIETY

Entered at Stationers' Hall, London

All Rights Reserved

MAILING DEPARTMENT IN THE NEW YORK OFFICES OF THE WESTERN ELECTRIC COMPANY

Authors and Collaborators

JAMES BRAY GRIFFITH, Managing Editor.

Head, Dept. of Commerce, Accountancy, and Business Administration, American School of Correspondence.

ROBERT H. MONTGOMERY

Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

Editor of the American Edition of Dicksee's Auditing.

Formerly Lecturer on Auditing at the Evening School of Accounts and Finance of the University of Pennsylvania, and the School of Commerce, Accounts, and Finance of the New York University.

ARTHUR LOWES DICKINSON, F. C. A., C. P. A.

Of the Firms of Jones, Caesar, Dickinson, Wilmot & Company, Certified Public Accountants, and Price, Waterhouse & Company, Chartered Accountants.

WILLIAM M. LYBRAND, C. P. A.

Of the Firm of Lybrand, Ross Bros. & Montgomery, Certified Public Accountants.

F. H. MACPHERSON, C. A., C. P. A.

Of the Firm of F. H. Macpherson & Co., Certified Public Accountants.

CHAS. A. SWEETLAND

Consulting Public Accountant.

Author of "Loose-Leaf Bookkeeping," and "Anti-Confusion Business Methods."

E. C. LANDIS

Of the System Department, Burroughs Adding Machine Company.

HARRIS C. TROW, S. B.

Editor-in-Chief, Textbook Department, American School of Correspondence.

CECIL B. SMEETON, F. I. A.

Public Accountant and Auditor.

President, Incorporated Accountants' Society of Illinois.

[iv]Fellow, Institute of Accounts, New York.

JOHN A. CHAMBERLAIN, A. B., LL. B.

Of the Cleveland Bar.

Lecturer on Suretyship, Western Reserve Law School.

Author of "Principles of Business Law."

HUGH WRIGHT

Auditor, Westlake Construction Company.

GLENN M. HOBBS, Ph. D.

Secretary, American School of Correspondence.

JESSIE M. SHEPHERD, A. B.

Associate Editor, Textbook Department, American School of Correspondence.

GEORGE C. RUSSELL

Systematizer.

Formerly Manager, System Department, Elliott-Fisher Company.

OSCAR E. PERRIGO, M. E.

Specialist in Industrial Organization.

Author of "Machine-Shop Economics and Systems," etc.

DARWIN S. HATCH, B. S.

Assistant Editor, Textbook Department, American School of Correspondence.

CHAS. E. HATHAWAY

Cost Expert.

Chief Accountant, Fore River Shipbuilding Co.

CHAS. WILBUR LEIGH, B. S.

Associate Professor of Mathematics, Armour Institute of Technology.

L. W. LEWIS

Advertising Manager, The McCaskey Register Co.

MARTIN W. RUSSELL

[v]Registrar and Treasurer, American School of Correspondence.

HALBERT P. GILLETTE, C. E.

Managing Editor, Engineering-Contracting.

Author of "Handbook of Cost Data for Contractors and Engineers."

R. T. MILLER, JR., A. M., LL. B.

President, American School of Correspondence.

WILLIAM SCHUTTE

Manager of Advertising, National Cash Register Co.

E. ST. ELMO LEWIS

Advertising Manager, Burroughs Adding Machine Company.

Author of "The Credit Man and His Work" and "Financial Advertising."

RICHARD T. DANA

Consulting Engineer.

Chief Engineer, Construction Service Co.

P. H. BOGARDUS

Publicity Manager, American School of Correspondence.

WILLIAM G. NICHOLS

General Manufacturing Agent for the China Mfg. Co., The Webster Mfg. Co., and the Pembroke Mills.

Author of "Cost Finding" and "Cotton Mills."

C. H. HUNTER

Advertising Manager, Elliott-Fisher Co.

FRANK C. MORSE

Filing Expert.

Secretary, Browne-Morse Co.

H. E. K'BERG

Expert on Loose-Leaf Systems.

Formerly Manager, Business Systems Department, Burroughs Adding Machine Co.

EDWARD B. WAITE

Head, Instruction Department, American School of Correspondence.

Authorities Consulted

The editors have freely consulted the standard technical and business literature of America and Europe in the preparation of these volumes. They desire to express their indebtedness, particularly, to the following eminent authorities, whose well-known treatises should be in the library of everyone interested in modern business methods.

Grateful acknowledgment is made also of the valuable service rendered by the many manufacturers and specialists in office and factory methods, whose coöperation has made it possible to include in these volumes suitable illustrations of the latest equipment for office use; as well as those financial, mercantile, and manufacturing concerns who have supplied illustrations of offices, factories, shops, and buildings, typical of the commercial and industrial life of America.

JOSEPH HARDCASTLE, C. P. A.

Formerly Professor of Principles and Practice of Accounts, School of Commerce, Accounts, and Finance, New York University.

Author of "Accounts of Executors and Testamentary Trustees."

HORACE LUCIAN ARNOLD

Specialist in Factory Organization and Accounting.

Author of "The Complete Cost Keeper," and "Factory Manager and Accountant."

JOHN F. J. MULHALL, P. A.

Specialist in Corporation Accounts.

Author of "Quasi Public Corporation Accounting and Management."

SHERWIN CODY

Advertising and Sales Specialist.

Author of "How to Do Business by Letter," and "Art of Writing and Speaking the English Language."

FREDERICK TIPSON, C. P. A.

Author of "Theory of Accounts."

CHARLES BUXTON GOING

Managing Editor of The Engineering Magazine.

Associate in Mechanical Engineering, Columbia University.

Corresponding Member, Canadian Mining Institute.

F. E. WEBNER

Public Accountant.

Specialist in Factory Accounting.

[vii]Contributor to The Engineering Press.

AMOS K. FISKE

Associate Editor of the New York Journal of Commerce.

Author of "The Modern Bank."

JOSEPH FRENCH JOHNSON

Dean of the New York University School of Commerce, Accounts, and Finance.

Editor, The Journal of Accountancy.

Author of "Money, Exchange, and Banking."

M. U. OVERLAND

Of the New York Bar.

Author of "Classified Corporation Laws of All the States."

THOMAS CONYNGTON

Of the New York Bar.

Author of "Corporate Management," "Corporate Organization," "The Modern Corporation," and "Partnership Relations."

THEOPHILUS PARSONS, LL. D.

Author of "The Laws of Business."

E. ST. ELMO LEWIS

Advertising Manager, Burroughs Adding Machine Company.

Formerly Manager of Publicity, National Cash Register Co.

Author of "The Credit Man and His Work," and "Financial Advertising."

T. E. YOUNG, B. A., F. R. A. S.

Ex-President of the Institute of Actuaries.

Member of the Actuary Society of America.

Author of "Insurance."

LAWRENCE R. DICKSEE, F. C. A.

Professor of Accounting at the University of Birmingham.

Author of "Advanced Accounting," "Auditing," "Bookkeeping for Company Secretary," etc.

FRANCIS W. PIXLEY

Author of "Auditors, Their Duties and Responsibilities," and "Accountancy."

CHARLES U. CARPENTER

General Manager, The Herring-Hall-Marvin Safe Co.

Formerly General Manager, National Cash Register Co.

[viii]Author of "Profit Making Management."

C. E. KNOEPPEL

Specialist in Cost Analysis and Factory Betterment.

Author of "Systematic Foundry Operation and Foundry Costing," "Maximum Production through Organization and Supervision," and other papers.

HARRINGTON EMERSON, M. A.

Consulting Engineer.

Director of Organization and Betterment Work on the Santa Fe System.

Originator of the Emerson Efficiency System.

Author of "Efficiency as a Basis for Operation and Wages."

ELMER H. BEACH

Specialist in Accounting Methods.

Editor, Beach's Magazine of Business.

Founder of The Bookkeeper.

Editor of The American Business and Accounting Encyclopedia.

J. J. RAHILL, C. P. A.

Member, California Society of Public Accountants.

Author of "Corporation Accounting and Corporation Law."

FRANK BROOKER, C. P. A.

Ex-New York State Examiner of Certified Public Accountants.

Ex-President, American Association of Public Accountants.

Author of "American Accountants' Manual."

CLINTON E. WOODS, M. E.

Specialist in Industrial Organization.

Formerly Comptroller, Sears, Roebuck & Co.

Author of "Organizing a Factory," and "Woods' Reports."

CHARLES E. SPRAGUE, C. P. A.

President of the Union Dime Savings Bank, New York.

Author of "The Accountancy of Investment," "Extended Bond Tables," and "Problems and Studies in the Accountancy of Investment."

CHARLES WALDO HASKINS, C. P. A., L. H. M.

Author of "Business Education and Accountancy."

JOHN J. CRAWFORD

Author of "Bank Directors, Their Powers, Duties, and Liabilities."

DR. F. A. CLEVELAND

Of the Wharton School of Finance, University of Pennsylvania.

Author of "Funds and Their Uses."

THE ADVERTISING DEPARTMENT WHERE ARE ORIGINATED THE PUBLICITY CAMPAIGNS OF THE SHERWIN-WILLIAMS CO., CLEVELAND, OHIO

Foreword

With the unprecedented increase in our commercial activities has come a demand for better business methods. Methods which were adequate for the business of a less active commercial era, have given way to systems and labor-saving ideas in keeping with the financial and industrial progress of the world.

Out of this progress has risen a new literature—the literature of business. But with the rapid advancement in the science of business, its literature can scarcely be said to have kept pace, at least, not to the same extent as in other sciences and professions. Much excellent material dealing with special phases of business activity has been prepared, but this is so scattered that the student desiring to acquire a comprehensive business library has found himself confronted by serious difficulties. He has been obliged, to a great extent, to make his selections blindly, resulting in many duplications of material without securing needed information on important phases of the subject.

In the belief that a demand exists for a library which shall embrace the best practice in all branches of business—from buying to selling, from simple bookkeeping to the administration of the financial affairs of a great corporation—these volumes have been prepared. Prepared primarily for[9] use as instruction books for the American School of Correspondence, the material from which the Cyclopedia has been compiled embraces the latest ideas with explanations of the most approved methods of modern business.

Editors and writers have been selected because of their familiarity with, and experience in handling various subjects pertaining to Commerce, Accountancy, and Business Administration. Writers with practical business experience have received preference over those with theoretical training; practicability has been considered of greater importance than literary excellence.

In addition to covering the entire general field of business, this Cyclopedia contains much specialized information not heretofore published in any form. This specialization is particularly apparent in those sections which treat of accounting and methods of management for Department Stores, Contractors, Publishers and Printers, Insurance, and Real Estate. The value of this information will be recognized by every student of business.

The principal value which is claimed for this Cyclopedia is as a reference work, but, comprising as it does the material used by the School in its correspondence courses, it is offered with the confident expectation that it will prove of great value to the trained man who desires to become conversant with phases of business practice with which he is unfamiliar, and to those holding advanced clerical and managerial positions.

In conclusion, grateful acknowledgment is made to authors and collaborators, to whose hearty coöperation the excellence of this work is due.

Table of Contents

(For professional standing of authors, see list of Authors and Collaborators at front of volume.)

VOLUME I

| Administrative and Industrial Organization | By James B. Griffith | Page 11 |

| The Business Engineer—Preliminary Investigation—Charting the Organization—Organization of Business—Organization of Mercantile Business—Universal Application of Organization Principles—Departmental Authorities—The General Manager—Comptroller—Sales Division—Superintendent—Purchasing Agent—Employment Department—Charting Salary and Wage Distribution—Expense Distribution Chart—Arrangement of Plant—Factory Plans—Office Plans—The Committee System—The Suggestion Plan—Order Blanks | ||

| Advertising and Sales Organization | By James B. Griffith | Page 61 |

| Systems and Records—Designs and Cuts—Cut Indexes and Tracers—Records of Printing—Periodical, Street Car, and Outdoor Advertising—Rate Cards—Advertising Contracts—Checking Returns—The Sales Department—Branches—The Mail-Order Branch—Follow-up Systems—Personal Salesmanship Division—Routing Salesmen—Sales Records | ||

| The Credit Organization | By James B. Griffith | Page 127 |

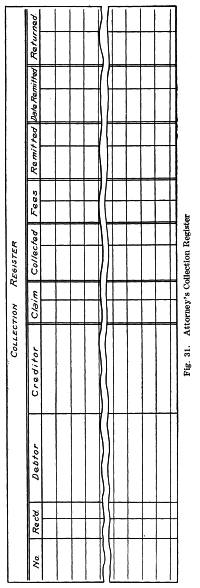

| The Credit Man—Information Required—Financial Statements—Analysis of Statements—Sources of Information—Local Correspondents—Credit Agencies—Recording Credit Information—Collections—Monthly Statements—Installment Collections—Collections by Attorneys | ||

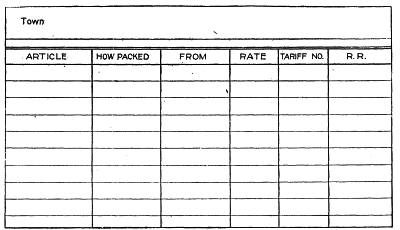

| The Shipping Department | By James B. Griffith | Page 183 |

| The Shipping Clerk—Class Rates—Commodity Rates—Freight Tariffs—Condensed Rate File—Routing Shipments—Filling Orders—Checking Shipments—Export Shipping—Freight Claims—Express Shipments—Retail Delivery System | ||

| Correspondence and Filing | By James B. Griffith | Page 231 |

| Opening and Distributing Mail—Correspondence Short Cuts—Talking Machines for Dictation—Copying Correspondence—Stenographic Division—Records of Work—Filing Division—Filing Systems—Methods of Indexing—Guiding, Transferring, and Sorting—Selecting Filing Equipment—Styles of Construction | ||

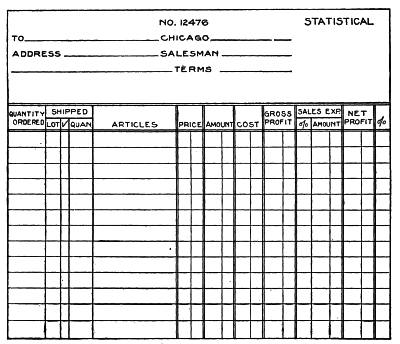

| Business Statistics | By James B. Griffith | Page 287 |

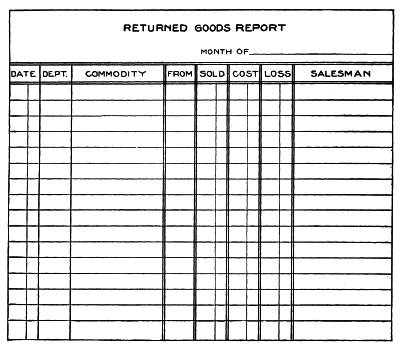

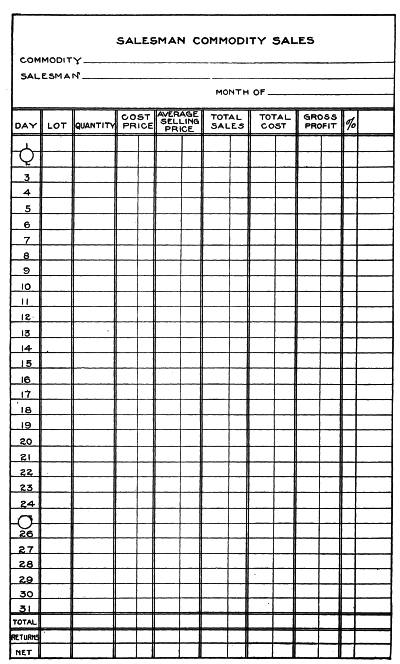

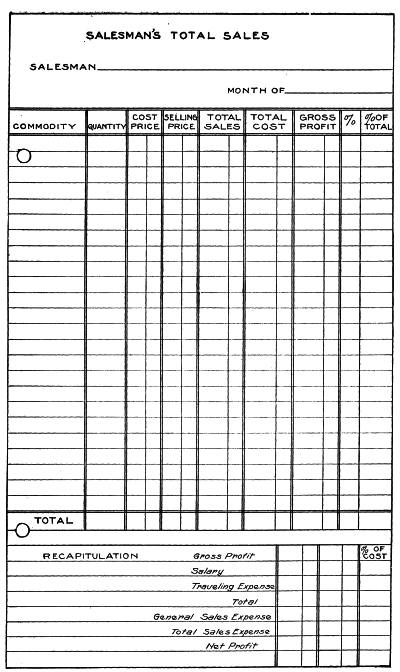

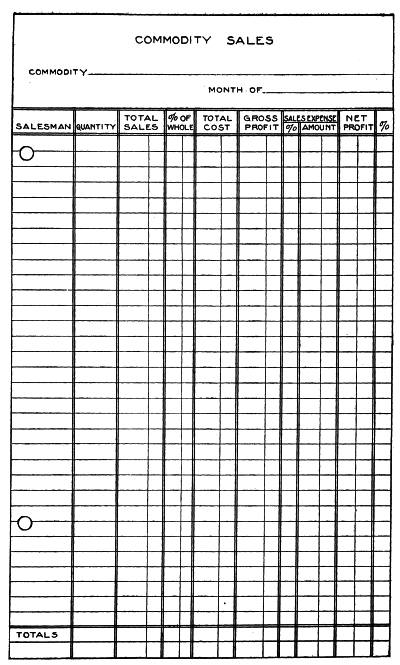

| Sales Costs—Records of Shipments—Returned Goods—Salesmen's Records—Expense Distribution—Department Sales—Trading Statements—Profit Figuring—Administrative Costs—Profit and Loss Statements—Mailing-Room Machinery | ||

| Review Questions | Page 333 | |

| Index | Page 347 | |

AN EXECUTIVE OFFICE AT THE PLANT OF CORBIN CABINET LOCK COMPANY, NEW BRITAIN, CONN.

ADMINISTRATIVE AND INDUSTRIAL ORGANIZATION

1. With little fear of contradiction, it may be stated that every commercial enterprise is conducted with the one purpose in view of making money for its owners. Naturally, the owners desire the largest possible returns from their investment of money or time, or both. Every person connected with the enterprise, in any capacity whatsoever, is indirectly working for the same purpose—to make as much money as possible for the owners of the business.

The largest possible volume of profitable business must be transacted; the business must be conducted with economy; the returns from each dollar expended must be as large as possible. This very condition is one of the beneficial results of modern business methods. The demand for a greater volume, lower cost of production, and more economical methods, has brought with it an incentive to greater effort on the part of the individual, with corresponding rewards.

That the efforts of the individual may be productive of best results, he must have the coöperation of other individuals engaged in the same enterprise. The enterprise must be properly organized.

Realizing the absolute necessity of harmoniously working organizations, keen students of business affairs have given much study to the question of how to organize a business. They have studied the plans of operation of the most successful enterprises, for the purpose of discovering those factors which have contributed most largely to their success. They have investigated and improved old plans and methods and invented new methods.

2. The Business Engineer. The investigations of these men have brought into being a new profession—that of the business organizer or business engineer—a profession that has quickly gained recognition. Business men, especially those at the head of large enterprises have not been slow to avail themselves of the services of men who have mastered the science of business organization.

For the same reason that he has long employed an architect to plan his building the modern business man calls in a business engineer[12] or systematizer, to perfect his business organization. As in every other profession, some incompetent men are found posing as business engineers, but an increasing number of trained men are entering the field. It is the work of these men that is placing the profession on a high plane.

The successful business engineer must have the ability to quickly grasp the plan of operation of any business with which his work may bring him in contact; he must be able to analyze conditions and to determine the factors which make for the success or failure of a business. His work is to organize and systematize every step of the work in every department.

3. The Preliminary Investigation. The first step in the organization or systematizing of a business is to determine its natural divisions. What is the nature of the business, and what are its distinguishing characteristics? Be it a manufacturing, jobbing, wholesale, retail, or professional concern, there is some one head on whom rests the final responsibility for the success or failure of the business. He must be surrounded with subordinates, each having certain duties to perform, who will be responsible for the performance of those duties, thereby coöperating to carry out the purposes of the enterprise.

The highest type of organization is found among the great industrial enterprises. These enterprises with their many activities most readily lend themselves to the application of scientific principles of organization. Here, organization can be carried to its final conclusion; in a smaller enterprise the same principles apply, but modification of details is necessary.

If we study the organization of a large enterprise, regarding it as a type, we can more readily grasp the requirements of a smaller business. But it must be remembered that in any event, the individual business must be studied and the organization made to fit the business. A tailor does not cut all coats from the same pattern.

In certain respects a great industrial organization may be likened to the army. At the head of the army is the commanding general, on whom rests the responsibility for the success of any campaign. He is surrounded by his staff, with whom he consults on questions of importance. When any important move is decided upon, the members of the staff—themselves in command of divisions of the army—issue[13] orders to their subordinate officers. They, in turn, pass the orders along, and at a predetermined moment, an entire army is set in motion.

Another important feature of the army organization which should be applied to the organization of a business is the disregard of the individual. Military authorities long since discovered that a high standard of efficiency could be maintained only through the organization of the army along certain lines. The question was not one of creating offices the duties of which would conform to the capabilities of certain men; the offices were first created, and then competent men were selected to fill them.

4. Individuals Disregarded. In creating responsibilities in a business organization, the individual should be disregarded, just as he is in the army. Unfortunately, the importance of this question is not always recognized. Too frequently the best interests of the organization as a whole are subserved to the interests of individuals. Business enterprises are organized and offices divided among the principal owners without seriously considering their respective abilities. This is wrong in principle, and works to the detriment of the business. It is one of the important problems to be solved in organization. Jones, who is a natural born financier, prefers to manage the selling end of the business, while Brown, a salesman of ability, is made treasurer. Neither is in the right place; change them about, and an efficient team would result.

Before we can perfect an organization, we must know what the business is. We must ascertain for what it is organized; what class of business is carried on; manufacturing, mining, jobbing, wholesale, retail, or a combination of two or more classes; whether conducted entirely in one plant or through branches; the method of marketing the goods; by traveling salesmen, agencies, or mail; the facilities for obtaining supplies, raw materials, or manufactured goods. When we understand the nature of the business, we are in a position to work out an impersonal, systematic organization.

Referring again to the necessity of a disregard of individuals in perfecting an organization, it is not the province of the business engineer to determine the qualifications of the men. He must be governed solely by the requirements of the business. When his work is completed, it is for the management to decide who is best fitted to assume[14] the duties and carry out the purposes of the departments and positions created.

We refer, for convenience, to the business engineer or systematizer; the principle is the same whether the one doing the work is acting in a professional capacity, perfecting the organization of his employer's business, or even solving the problems of his own establishment.

OBJECTS AND CHARACTERISTICS OF ORGANIZATION

5. To reduce the subject to concrete form, the objects of business organization may be defined as follows:

| (A) | To unite the individuals who are to conduct an enterprise into a body which will work systematically to a common end. |

| (B) | To bring together or group the component parts of the body with respect to their specific relations and duties. |

| (C) | To elect officers and appoint committees and authorities with clearly defined duties and responsibilities. |

These definitions all lead to a common center, that is, coöperation. Without co-operation the success of any organization is very questionable, if not impossible. With it—a body of men all working together for a common end—almost any apparent obstacle will be surmounted. No matter how large an organization may be, how many or wide its ramifications, if the spirit of co-operation prevails, it will move as one irresistible body.

And, regardless of the size or nature of a business enterprise, the organization, as here used, resolves itself into certain easily distinguished components, as follows:

First: The owners, represented in a corporation by the stockholders or investing public; in a partnership, by the partners; in an individual business, by the proprietor.

Second: The executive or managerial division.

Third: The commercial or active business division.

Fourth: The manufacturing or productive division.

These components lend themselves naturally to certain specific subdivisions; natural groups are formed to insure efficient management; certain authorities are delegated to effect economical operation.

The stockholders (owners) first elect from among their number, a board of directors. This is the initial step toward perfecting a business organization. The directors represent the stockholders,[15] and the interest of the stockholder, as such, becomes that of an investor only. His interest in the operation of the business is to be looked after by the directors, whom he, or a majority, has elected.

From this board of directors is built the framework of the executive or managerial division. The first act of the directors is to meet and elect the usual executive officers: President, Vice-President, Secretary, and Treasurer. In modern organizations, it is customary to also elect or appoint an executive committee or board of managers.

This committee consists of three or more members, usually selected from the officers, to which may be added one or more directors who are not officers.

To this committee, the board of directors delegates its authority in the actual conduct of the business. This plan of electing an executive committee is particularly desirable when the board is a large one, as it concentrates authority and results in more prompt action on matters demanding immediate attention. A large body is unwieldy, a quorum cannot always be brought together on short notice, but a working majority of a small committee can be convened promptly.

The executive committee takes charge of both the commercial and manufacturing divisions. To still further concentrate authority, it is customary to appoint a General Manager who has direct supervision over the immediate operation of both commercial and manufacturing divisions. He is appointed sometimes by the executive committee, but more often by the board of directors.

The general manager, while occupying a position of chief acting executive, acts with the executive committee and is directly responsible to the board of directors.

The commercial division of a business naturally subdivides into two sections: Accounting, and Advertising and Sales. The first thought of the student might be that accounting is given a position of too great importance, but in the sense here used it means the records of the business of every nature, the accounts, the gathering and recording of statistics and information of every character.

The manufacturing division divides into Purchasing and Stores, and Production. In a measure, the purchasing of goods is a function of the commercial division, but the purchasing of raw material and supplies is properly under the supervision of the manufacturing division.

CHARTING THE ORGANIZATION

6. What may be termed the anatomy of an industrial body, is most graphically shown by means of charts. Free use of charts will be made throughout these papers. With properly designed charts the logical divisions of authority or expense can be clearly shown.

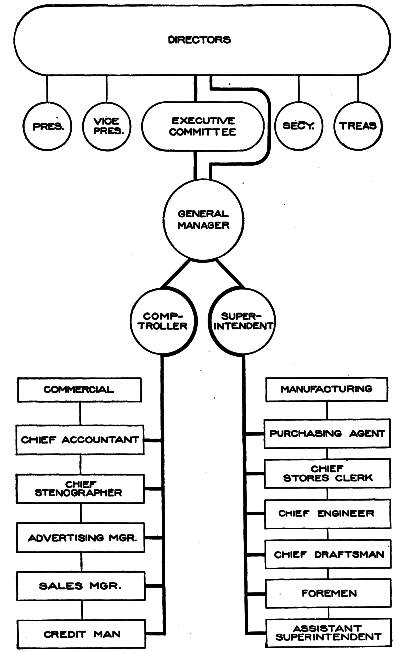

Fig. 1 furnishes a graphic illustration of the principal components of the organization under discussion. In the first group we find the owners (stockholders) whose line of communication with the business is through the board of directors. Subordinate to the board of directors are its own executive officers, the executive committee, and general manager.

The connecting lines show the executive committee to be in direct communication with the board of directors, while the general manager is in direct communication with both the executive committee and the board of directors.

Under the general manager are the commercial and manufacturing divisions, over both of which he has direct supervision.

7. Working Authorities in Large Enterprises. The next logical step in the development of our organization is a study of the working authorities and responsibilities of the different officers and their assistants. We have seen that the administrative authority is for practical purposes centered in the general manager. It is not to be supposed, however, that in a large industrial organization he will personally supervise all of the details of operation of the commercial and manufacturing divisions. His time must not be taken up with details which can be as well handled by subordinates. He should be free to devote his time to questions of policy, the providing of finances, the consideration of new fields of endeavor, and the making of the more important contracts. His immediate assistants will be a Comptroller and a Superintendent.

The comptroller fills a position identical with that of a business manager or an assistant manager. His duties are mainly in connection with the commercial division. It is his business to devise systems of accounts and systems for recording the activities of every department, and have reports compiled, in proper form for presentation to the general manager. His is a statistical department, filling a place between the general manager and the subordinate departments, and, while not closing the avenues of communication between these departments and the general manager, it is here that reports and records of results are concentrated.

Fig. 1. Chart of a Corporate Manufacturing Enterprise

The superintendent is in immediate charge of manufacturing operations and is responsible for the custody of all property used in manufacturing. His position does not close the avenue of communication between factory departments and the general manager.

Fig. 2 illustrates the subdivisions of the commercial and manufacturing branches. This chart does not go back of the administrative section of the organization, as the stockholders have no direct connection with the actual operation of the business.

We find the subdivisions of the commercial branch in charge of the following: Chief Accountant, with direct supervision over all bookkeeping and accounting records; Chief Stenographer, in charge of all stenographic and circularizing work; Advertising and Sales Managers, in charge of publicity and selling campaigns; Credit man, in charge of credits and collections.

The manufacturing department includes the Purchasing Agent, who purchases all manufacturing stores, materials, and supplies; Chief Stores clerk, in charge of the storage of all materials and supplies; Chief Engineer, who designs new products, new machinery for the manufacture of that product, and conducts all experimental work; Chief Draftsman, who superintends the work of the drafting rooms; Assistant Superintendent, in charge of maintenance of power and heating plants, internal transportation facilities, machinery and buildings; Foremen, in charge of shops employed in production work.

As shown by the lines of communication, represented by the heavy lines, the authorities of the comptroller and superintendent extend to every phase of the work of the commercial and manufacturing branches. The comptroller is in communication with the manufacturing branch since the making of schedules, time keeping, and the assembling of cost statistics are all centered in his office. He does not, however, assume any of the duties of the superintendent, and while their work is closely related, the two officers conduct their departments without conflict of authorities. It must be remembered that they are equally responsible to the general manager, which of itself requires cordial coöperation.

Fig. 2. A Chart of Working Authorities in a Manufacturing Business

8. Organization Applied to Small Business. We have referred only to large manufacturing enterprises divided into many departments, necessitating a division of executive duties among a large number of minor executives. While, in the organization of a smaller enterprise, not all of these department heads will be required, the principles of organization, so far as division of authority is concerned, remain the same.

In the small corporation, we find the same board of directors elected by the stockholders. This board may be small, consisting of no more than five, or even three members, but the same executive officers are elected. One man may hold more than one office, as secretary and treasurer, or vice-president and treasurer, yet each office is filled. If the board is small the executive committee may be omitted, in which case the board itself performs the duties of the executive committee. There is the same general manager; at least the duties exist even though there be no such office in name. The president may act as the executive head, and be recognized as the actual manager of the business, but in so doing he is acting in an entirely different capacity than that pertaining to the office of president.

Extending the illustration to a small manufacturing enterprise, the general manager may assume all of the duties of the comptroller in the operation of the commercial branch; he may be his own sales manager or credit man; or in the manufacturing branch, he may act as superintendent.

The treasurer of the corporation may be the accountant and also act as credit man. The advertising and sales managers may be one, or the superintendent may be the purchasing agent as well.

The point intended to be emphasized is that there are certain duties to be performed, certain responsibilities to be met, certain authorities to be assumed even though it be but a one-man business. And in this is illustrated the importance of creating any business organization without regard to individuals.

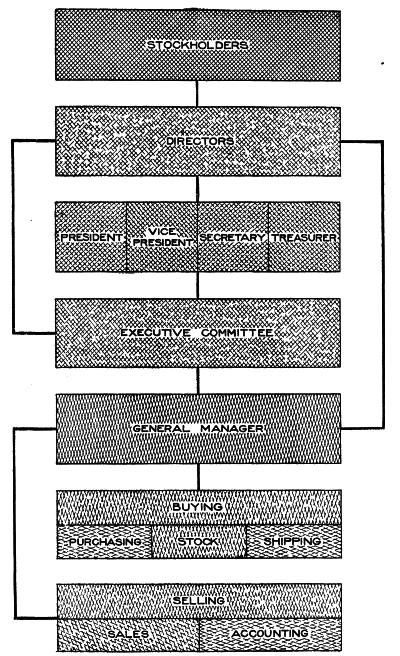

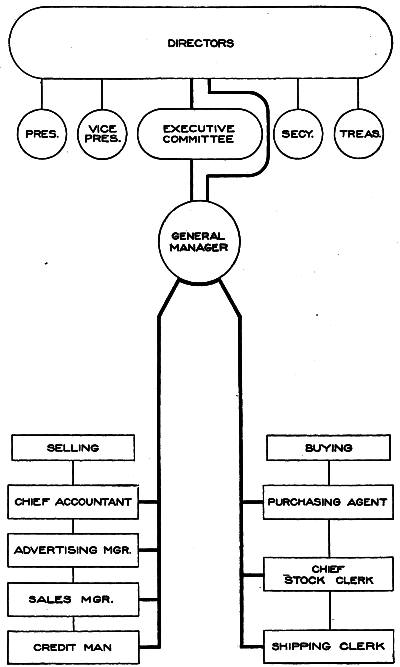

9. Organization of Mercantile Business. Leaving for a time the organization of a manufacturing enterprise, we will consider the application of the principles of organization to a trading business. In such a business, the administrative section remains the same: stockholders, directors, officers, executive committee, general manager. At this point the business naturally divides into the departments of buying and selling.

Fig. 3. A Chart of a Corporate Trading Enterprise

The buying department is subdivided into purchasing, stock, and shipping. The subdivisions of the sales department are sales and accounting. Our chart of the organization shown in Fig. 3, follows the same lines as Fig. 1, the only change being in the main divisions.

Advancing the next step we find the executive officers in charge of the several divisions of the work, corresponding very closely to those shown in Fig. 2. The buying department is in charge of the Purchasing Agent, Chief Stock Clerk, and Shipping Clerk, or Traffic Manager, as he is sometimes known.

The selling department is in charge of the Chief Accountant, Advertising Manager, Sales Manager, and Credit Man. This is shown clearly in the chart, Fig. 4.

Lest an erroneous impression be gained, it may be well to state at this point that the advertising and sales managers must work in perfect harmony. Indeed, advertising is one branch of the sales department and the success of one is so closely interwoven with the other that no important step should be taken by either independently.

In many large concerns, the sales manager is the real advertising manager, even though another may supervise the actual routine of preparing advertising matter. A competent advertising man makes a successful sales manager, and every sales manager should have advertising training, for the purpose of advertising is to create a demand and assist in making sales.

Referring again to Fig. 4, it is seen that both buying and selling departments are under the control of the general manager, from whom direct lines of communication lead to every division of these departments. Direct communication is also maintained between the two departments. The accounting division keeps the accounts of the buying department; the sales division must be in communication with the purchasing and stock division in respect to maintaining the stock to be sold, and with the shipping division in respect to the filling of orders.

10. Universal Application of Organization Principles. When we go into all of the ramifications of business we find many establishments where minor variations of our plan of organization appear necessary, but in the final analysis, the fundamentals prove to be the same.

Fig. 4. Chart of Working Authorities in a Trading Business

Reduced to its simplest form, we will suppose the business under consideration to be a small retail establishment conducted by two partners. No thought has been given to the principles of organization, yet they are applied in that little store just as surely as in the immense manufacturing plant.

Ask any commercial salesman calling on the firm who is the man to see regarding the introduction of a new line of goods, and he will probably answer, "Mr. Jones is the man to see; he does the buying." With no thought of organization, the owners of this little business realize that it is best for one man to do the buying. Perhaps the other may inspect samples, his opinion may be asked, he may even place an occasional order, but it is not the rule of the establishment. By placing the buying in the hands of one partner, confusion is avoided. He can keep in closer touch with prices, and the results are far more satisfactory.

Advancing to the larger retail business of the department store, whether the general store of the small town or the big store of the city, we find a different problem. Here the buying is further specialized, for one man buys for one, or at most three or four departments. The same men act as sales managers and buyers in the departments for which they are responsible. The manager of a department in a big store is selected as much for his ability as a buyer as for his salesmanship. But we do not get away from fundamental principles, for in buying and selling the manager is performing two entirely separate and distinct functions.

No matter what the business, we find the same two fundamental functions, that is, buying and selling. As illustrations of the application of this principle to different businesses we give the following:

Publishers of newspapers and other periodicals buy editorial work, manuscript, engraving, paper, printing; sell subscriptions, advertising space.

Publishers of books buy editorial work, manuscript, engraving, paper, printing; sell books.

Railroad companies buy equipment, rails, lumber, coal, supplies, labor; sell freight and passenger transportation.

Schools and colleges buy textbooks, supplies, services of instructors; sell instruction.

Professional men buy their instruction, books, instruments, office furnishings, clerical assistance; sell their services.

In every undertaking, revenues are produced through salesmanship. Every business and every profession has something to sell,[25] and its financial success depends largely upon the quality of salesmanship employed. Whether it be a professional man with nothing but his services to sell and no other means of advertising than through work well done, or a gigantic commercial organization with its extensive advertising campaign and many salesmen, a selling organization exists in some form. And before anything can be sold it must be procured, or bought.

On this question of the universal application of the principles of organization, we quote from a valuable contribution in The Engineering Magazine, by C. E. Knoeppel:

"While business as it is now conducted is not as simple as it was in the barter days, it must not be inferred that this segregation of authority is synonymous with complexity, for its very purpose has been to simplify, and that is what it has accomplished. It is only where this segregation has been the result of lack of thought and proper attention, or other like causes, that we find a complex and unsatisfactory condition of affairs. In fact, there is all about us sufficient evidence that many commercial enterprises are being conducted along lines that, as far as evolutional development is concerned, are several stages behind the times.

"Let us suppose a case, which will apply in a greater or less degree to the majority. In the earlier development, we will say that the founder of the business was able, on account of its small size, to make what sketches he needed, solicit orders, see that they were filled, perhaps take a hand at the making if occasion required, see to the shipments, and attend to the collections and the keeping of his few accounts. He finds that the business grows, and eventually places a man in charge of certain branches while he looks after others. The accounts eventually require more attention than he can give them so he engages a bookkeeper in order that he may be relieved of the work. He finds that the quantity of materials received and shipped amount to enough to warrant a receiving clerk as well as a shipping clerk, and, to handle this material from its inception to shipment he conceives the idea of placing a man in charge as stock clerk. He then adds a purchasing agent, in order that he may be relieved of the detail and that purchases may be made most economically; a man is placed in charge of the orders; foremen are placed in charge of certain men in the shops; the details connected with making plans, drawings, estimates, etc., are taken over by a practical man; his manager is given a man to look after the shops or engineering branch; while the commercial branch with its many details is placed in the hands of another. As the evolution continues, the selling branch is assumed by one man; cost details are looked after by another; a chief inspector is added in order that all work may be shipped according to specifications; the engineer, who before had been a sort of jack of all trades, is placed in charge of certain work, while an electrician is engaged to look after this particular work; and so this segregation continues as the development continues.

"Perhaps it is not to be wondered at that the founder, in looking backward, is inclined to pat himself on the back when, in a reminiscent mood, he[26] considers what he terms 'remarkable development.' He considers that he has been wonderfully successful in building up a business which at the beginning was so small as to admit of his supervising every detail, while today he employs a dozen men to do the work he once did. There is no getting away from the fact that it is this same feeling of self-satisfaction that is responsible for a large number of faulty organizations, for if we should tell this manufacturer that his business is far from being as successful as it is possible for it to be ... he would vigorously resent any such accusation; but the fact remains that it is not the success it should be, for the very reason that the development has been allowed practically to take care of itself. New men were added, new offices created, only when absolutely necessary, each newcomer being given a general idea of what was expected of him, and not knowing, not thinking, or perhaps not having the time to give more than passing attention to the matter, the proprietor did not consider the fact that his business was a unit, with each worker a part, having a distinct relation with every other worker. Hence, as the efficiency of any organization is directly in proportion to the care with which these relations are considered and treated, his organization naturally fails to attain that degree of efficiency obtainable, and for this condition he, and he only is responsible."

11. Departmental Authorities. The next logical step in the development of our organization is an analysis of the departmental organizations. We have seen how the operations of the business are divided among several divisions or departments. The reason for such divisions is apparent. In a large business no one man can personally supervise all of its activities. Each division is engaged in certain activities that demand the immediate supervision of specialists. One man is a specialist in advertising, another in sales plans, others in purchasing, specific manufacturing operations, or the design and maintenance of appliances intended to improve the product or to reduce costs.

To reach the highest state of efficiency in every department of the business, these specialists must be employed, which is another reason for organizing a business along the line of its activities, and without respect to individuals.

Before we can decide what manner of man should be placed at the head of this or that department, we must study the duties of the position, the responsibilities involved, the authorities to be assumed. To present this problem in graphic form, the chart (Fig. 5) is designed. While the arrangement is not inconsistent with Fig. 2, this chart of the same class of organization is laid out along the lines of authority. It shows both the authority of the department head and the necessary activities of his division.

We have selected the organization of a large industrial establishment for the very reason that many divisions and departments are necessary. The smaller organization will have a less number of divisions, but it is much easier to condense than to expand a given plan. Any man who understands the requirements of a large organization can readily adapt those ideas to a smaller establishment. He can apply the plan so far as it can be used to advantage. Some variations of the application of the plan will be pointed out in our departmental analysis.

Fig. 5. A Chart Which Shows the Duties, Responsibilities and Authorities to be Assumed by Each Department Head

It is perhaps unnecessary to say that while the authorities of some of the department heads have been referred to in preceding[28] pages, this analysis is intended to exhibit these authorities in greater detail.

12. General Manager. As a rule the general manager has general supervision over the commercial and manufacturing branches. In conjunction with the president and executive committee, he formulates all policies to be followed in purchasing, manufacturing, sales, and advertising, establishing credits, and accounting methods. He is responsible to the executive committee and board of directors for procuring materials, their manufacture and sale, and the maintenance of buildings and machinery.

It is his duty to keep in touch with the operations of every department and to post himself on the general efficiency of all classes of workmen. Through reports he will keep informed in regard to the results of the operations of every department.

While in direct communication with all department and division heads, he will have for his immediate assistants, a comptroller and a superintendent. It is from the comptroller that he will receive statistics and reports of the activities of the business in all its branches, while to the superintendent he delegates his authority in the actual operation of the manufacturing branch.

13. Comptroller. "A controller or manager" is a standard definition of the term comptroller. In the organization under consideration, he is a controller of the business by virtue of the fact that he is responsible for the accounting and recording of all activities of the business.

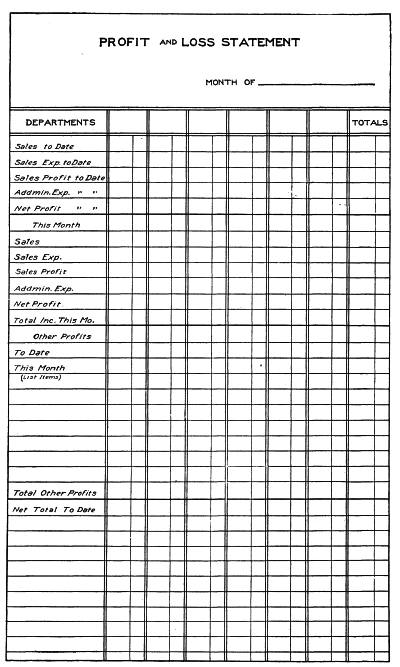

He occupies the position of auditor and is the real systematizer of the business. He creates all systems of commercial accounting, cost accounting, departmental records, time keeping, and pay rolls, reports of superintendent, perpetual inventory, sales statistics, and, in fact, all records of the business. He prepares all balance sheets, comparative statements, trading, manufacturing, and profit and loss statements, and reports to the general manager or executive committee, or both, on the condition of finances, materials, and finished goods.

Since the formation of important policies may hinge on the reports and statistics of his department, he occupies an office next in importance to the general manager. The training and experience gained in his office place him in direct line for promotion to the office of general manager.

His authority is absolute over the accounting and stenographic departments, while his authority extends to other departments only in respect to their record systems. In the accounting department, his direct assistant is the chief accountant; and in the stenographic, the chief stenographer.

In a smaller organization the comptroller may not require the services of a chief accountant, in which case he performs the duties of the position. Or the treasurer may occupy the office of comptroller.

Chief Accountant. The chief accountant is in immediate charge of the commercial and factory accounting. His assistants are cashier, bookkeepers, factory accountant, cost clerks, time clerks.

This department accounts for the receipt and disbursement of all moneys and properties, figures costs and pay rolls, and prepares statistics necessary for the use of the comptroller in making up his reports and statements.

It is evident from this that the comptroller is in a sense the custodian of all property belonging to the business, since he must, through his accounting department, account for its receipt and disbursement. This explains why the comptroller prescribes all systems for the care and recording of stores, supplies, and finished product.

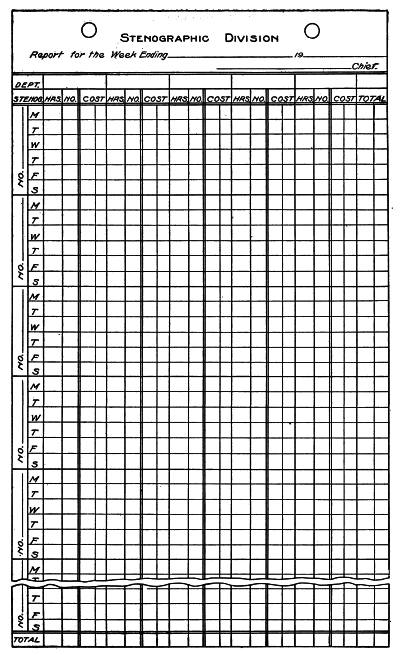

Chief Stenographer. The chief stenographer is at the head of the correspondence department, with authority over all stenographers, typists, filing and mailing clerks.

Stenographers are supplied to all divisions by this department. This plan of having all stenographers in one department subject to the call of those having need of their services is now adopted by most large concerns, except in a few cases where stenographers act as private secretaries to the officers. The plan is an economical one, for only the number actually required to handle the work of the establishment need be employed. Under the old plan of employing one or more stenographers in each department, it is common to find them idle in one department while in another the work is behind. Another strong point in favor of the more modern plan is that each stenographer becomes familiar with the dictation of all departments, and no stenographer has an opportunity to become familiar with the secrets of the business.

In the stenographic department, the work of addressing and mailing form letters, catalogues, and circulars is done.

All correspondence is filed by this department.

Records of office supplies, stationery and printed matter are maintained in this department.

The chief stenographer has charge of and accounts for all postage, but secures postage by requisition from the cashier or accountant.

14. Sales Division. By far the most important division of the entire commercial branch is the sales division. This division is responsible for finding a market for the output of the business.

It must create a demand for the product through advertising, open new fields, study the demands of the trade and the products of competitors, ascertain as far as may be the possibilities of marketing new products, and, above all, sell goods at a profit.

The selling division of some of the largest industrial establishments is in sole charge of a general sales manager, who has authority over the advertising as well as selling. In our chart we have divided responsibility for the conduct of this division between sales and advertising managers, placing the advertising manager on an equality with, rather than subordinate to, the sales manager. This combination will produce the most satisfactory results for most enterprises.

Advertising Manager. The advertising manager has charge of the preparation of all advertising literature, catalogues, copy and designs for all periodical advertising and usually the placing of all contracts for printing and engraving.

He has authority over all artists and copy writers employed regularly and for special work.

With the sales manager and general manager, he makes up appropriations for periodical advertising and places contracts when these appropriations have been approved.

He confers with the sales manager on all questions pertaining to his work, no printed matter for the use of the selling division being ordered until approved by the sales manager. Thus, coöperation of the sort that makes for success is assured.

Sales Manager. The sales manager has authority over the sale of goods and filling of orders, and his department is divided into selling and filling. The selling department is further subdivided into salesmen and mail orders.

One subdivision represents that portion of the sales made by personal salesmen. The active work is carried on by salesmen who call on the trade under the orders of the sales manager.

The sales manager hires all salesmen, prescribes their territories and routes, and supervises their expense accounts.

He compiles reports and statistics of their work for presentation to the comptroller or general manager, and keeps the records prescribed for this department.

The mail order division is engaged in the sale of goods by the use of letters, circulars, and catalogues. Lists of customers and prospective customers are maintained, and sales follow-up systems are operated under the immediate supervision of this division.

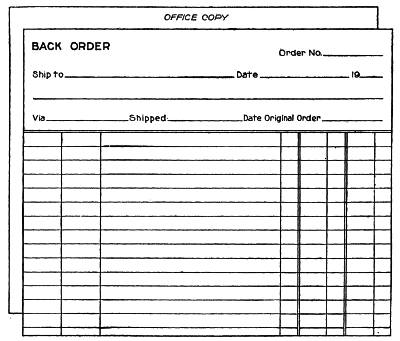

In the filling department, the chief order clerk is in charge of entering sales orders, making shipping orders and manufacturing orders. He maintains a record of sales and manufacturing orders so that he can keep informed on manufacturing or stock requirements. All invoicing of shipments is done in this department.

The shipping clerk maintains records of rates of transportation by rail, water, or truck, and keeps posted on routes and facilities. He supervises the packing of all goods, and secures proper receipts from transportation lines.

Credit Man. The position of the credit man is an important one in any establishment.

He collects and records information about the financial responsibility and credit standing of customers. When necessary, he makes special investigations, and on the basis of his information extends or limits credit. Every order from a new customer must be approved by the credit man before it can be accepted.

When accounts have been opened, it is the duty of the credit man to collect them when due, or, if not paid promptly, to use every means to secure a settlement. His work brings him in contact with both the sales and accounting departments.

The credit man is assisted by such clerks and collectors as may be necessary for the conduct of his department.

15. Superintendent. The superintendent is given general supervision over the manufacturing branch of the business. His authority extends directly to the engineering and drafting departments, the work of the assistant superintendent, foreman of tool room, and shop foremen. His relations with the purchasing department are advisory rather than managerial.

His immediate assistants are the chief engineer, assistant superintendent, and shop foremen.

It is his duty to execute orders for the manufacture of goods, operate the plant in the most economical manner, study and introduce processes and methods that tend to reduce manufacturing costs, and keep informed generally on the efficiency of men, machinery, appliances, and materials in all manufacturing departments.

With the assistance of the purchasing agent he provides all materials and supplies required in the manufacture of goods or for the operation of the plant.

Chief Engineer. The chief engineer designs all special machinery and appliances to be manufactured for use in the plant, designs and plans all new products for which there appears to be a demand, and personally supervises the experimental department. The installation of new equipment is also done under his supervision.

His authority extends to the drafting department which is in charge of a chief draftsman. This department draws all designs, plans of new machinery or product, and all plans not classed as architectural.

In a plant where many special tools are made, the chief engineer also has authority over the tool room.

Assistant Superintendent. The assistant superintendent is responsible for the maintenance in efficient condition of all power, pumping, heating, and lighting plants, internal transportation facilities, and the repair of buildings and equipment.

Except in the larger plants, he has authority over the tool room which is placed in charge of a tool room foreman. This department is responsible for the custody of all tools, repairs to tools, and their manufacture. Tools are issued only on requisition and perpetual inventories are maintained according to systems prescribed.

In some very large industrial plants, like a steel plant, there are several assistant superintendents, each having specific duties. There may be a superintendent of power, superintendent of transportation, superintendent of machinery, superintendent of buildings, superintendent of stores, etc. In a small plant, the superintendent will personally perform the duties here assigned to the assistant superintendent.

Shop Foremen. As the name indicates, the shop foremen are in charge of the various shops or manufacturing departments. It is the duty of the shop foreman to lay out the work called for by the[33] orders of the superintendent, and to assign the work to his men. He will make provision for the prompt execution of orders by making requisition for the number of men that can be profitably employed in his department. It is his duty to keep all of his men supplied with work.

16. Purchasing Agent. The purchasing agent has charge of the purchase of all materials for the manufacturing branch, and in some cases for the commercial branch. In a purely trading concern, his duties would be in connection with the commercial or selling branch, but in a large industrial enterprise, the purchase of office supplies, advertising literature, etc., is usually under the supervision of the comptroller, chief accountant or advertising manager.

He procures catalogues, price lists, names of manufacturers and dealers, and keeps generally informed as to sources of supply. He obtains samples which are submitted to tests by the engineering department or otherwise.

With the superintendent and general manager, he makes schedules of materials, secures bids, and places orders. Records of orders and all information needed in his office are kept according to the systems prescribed by the comptroller.

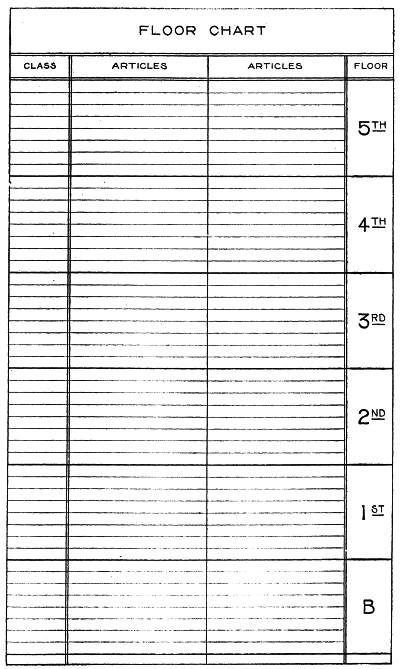

He has full authority over the store rooms, in which he is assisted by the chief stores clerk. This department receives all goods, checks receipts with orders or invoices, stores the goods, delivers them on properly executed requisitions, and maintains perpetual inventory records as prescribed.

EMPLOYMENT DEPARTMENT

17. A department, or rather a sub-department, not shown on the chart but found in some establishments, is the employment department. This department is very properly in immediate charge of the superintendent, and, in the average manufacturing plant, he will hire all men. In a plant employing a great number of men, it is impossible for the superintendent to personally take charge of this work, and an employment agent is placed in charge.

The employment agent keeps records of all employes and applicants and hires all men needed by the different foremen.

GENERAL MODIFICATIONS

18. The organization that we have described is a representative illustration of the application of the principles to a large enterprise,[34] necessitating a considerable number of subdivisions. But even here the charts show only what may be termed the principal divisions; the charts might be extended in greater detail. The explanation might include the exact duties of every employe in each department, but, as our purpose is to present general principles in sufficient detail to serve as a guide, explanations of these minute details have been omitted.

There are, however, modifications to be found in certain cases which may be made clear by further suggestions. We have referred to the comptroller, and while in many concerns no such office is recognized, at least by that title, some man in every business of any magnitude fills an analogous position.

Most frequently it is the auditor, or if the office of auditor has not been created, it may be the treasurer. Again, the duties or a greater part of them, may fall on the office manager or the chief accountant. Even in a small partnership where one of the partners is the bookkeeper, the duties exist, and are performed by that partner who keeps the accounts. It must be remembered that the comptroller's office is primarily statistical. It matters not whether the statistical operations involve the keeping of a simple set of books or require large commercial and factory accounting forces with a third division to compile statistics from their records, every business demands certain statistical work. Neither is it important whether the man in charge of this work be called comptroller, auditor, accountant or office manager, but we have used the title of comptroller as more exactly descriptive of the functions of the office when carried to its legitimate conclusion in a large business.

While, in most manufacturing industries, the superintendent and purchasing agent have full authority in the making of purchases for the manufacturing branch, it has been found advisable in some cases to give the comptroller authority over the purchasing department. A reason for this is the importance of reducing the investment in raw material, supplies, etc., to the lowest point consistent with the actual requirements of the business. Much needless capital is tied up in raw material, when it might be at least earning bank interest. His chief concern being to provide a liberal supply of raw materials, the superintendent is very liable to overstep the bounds in the direction of too liberal purchases.

A still different condition is found in a large merchandising establishment. Here practically every department manager is his own buyer and while he must be regarded as the best judge of what to buy, it becomes necessary to supervise his purchases in respect to quantities. The comptroller should, therefore, have authority over the amounts invested by the several buyers. This is usually controlled by giving the buyer a stated appropriation at the beginning of each season, the amount being determined by a study of present conditions and records of past performance. The making of an appropriation does not operate against special appropriations to be used in taking advantage of specially advantageous market conditions, or to increase stocks of fast selling lines.

DUTIES CLEARLY DEFINED

19. One of the first requirements in the development of a successful organization is that the duties of every employe be clearly defined, and that each employe be fully informed as to his duties. Nothing tends to produce greater friction than an overlapping of duties and authorities.

In a manufacturing plant, when a foreman is placed in charge of a shop he should be instructed as to his authority, responsibilities, and exact duties. When these authorities have once been established, no other man of equal or lower grade in the organization should be permitted to interfere in any way, nor should the foreman be permitted to overstep his authority.

Those occupying positions to which greater authorities are attached should also be careful to not presume upon their authority by attempting to direct work properly under control of the foreman. The superintendent or manager who, in passing through a plant, discovers a workman in the act of violating an established rule, or doing something dangerous to the lives of himself and fellow employes, or performing work in the wrong way, is justified in at once bringing the matter to the notice of that workman; but he should report the occurrence to the foreman at the first opportunity.

On the contrary, if the manager or superintendent wishes to make a change in policy involving a departure from the established customs of the shop, or if he requires the services of a workman even temporarily in another department, he should first take up the matter with the shop foreman.

The same policy in general should be observed throughout the organization. The person placed at the head of a department or division of the work should have full authority and be held responsible for the work of all employes in that department. Complaints of inefficiency of an individual employe should be made to the department head. If the purchasing agent, for instance, finds the work of a certain stenographer unsatisfactory, his complaint should be made to the chief stenographer.

20. Duties of Individual Workmen. The duties of the individual workman in the shop should be as clearly defined as are those of his foreman. It is the duty of the foreman to lay out the work and to keep the workman regularly employed on the work assigned to him.

In the operation of the manufacturing branch, the most important consideration is economy of production. When a workman is kept at one task he becomes a specialist, increases his production, and reduces costs.

21. Duties of Office Employes. Each clerk in the office should have his work clearly defined. If specialization is profitable in the shop, it is equally so in the office. Every man who has been responsible for the management of an office will agree with us that in no other branch of business is there a greater tendency to allow work to get behind.

Lack of system is mainly responsible for this state of affairs. While his duties may be more or less clearly defined, the work of the average office clerk does not follow any well defined plan. He does the thing that seems most important, leaving the less important tasks until he "has time." Instead of surveying the field and laying out a logical, systematic plan, the average office employe goes about his work in a haphazard sort of way following the line of least resistance.

The work in every office is largely routine, but the faithful performance of routine tasks is a necessary accompaniment to those larger tasks, which in themselves, appear of greater importance. Routine tasks are drudgery—something that every man seeks to escape. In freeing himself from a state of drudgery, the department head should be careful lest he place his subordinates in the same dreaded rut. An office clerk should be given an opportunity to learn all of the routine of the division in which he is employed. He will become a more valuable employe; while adding variety, the performance of more than one task is training him for a more advanced position.

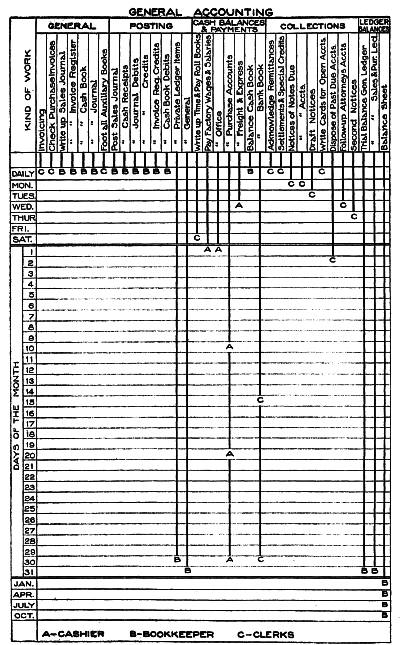

Fig. 6. A Working Chart for the Guidance of the Employes in One Department

To properly systematize the routine, the department head should first study his department to find out what the routine tasks really are—what work must be done each day or each week. He should then list these tasks and assign them to certain clerks to be performed at certain stated times.

This can be best presented by means of a chart as shown in Fig. 6. This chart covers the work of a typical general accounting department. At the top, the general or routine tasks are listed, grouped under proper divisions. From each task listed a line is extended to the time when it is to be performed: daily, the day of the week, day of the month, or the month. The letters at the end of the lines indicate by whom the tasks are to be performed, C representing clerks, B, bookkeepers, and A, cashier.

Taking the collection division as an illustration, we will suppose that it is Monday, the 2nd of the month. The chart shows that on Monday notices of notes and accounts due are to be mailed. On the second day of the month, past due accounts must be taken up and disposed of. In addition are the daily tasks as indicated by the lines extending to the daily line.

When a task is to be performed two or three times in a month, the line is broken and the letter inserted at each break. Even the time of drawing off a balance sheet, once every three months, is indicated. A similar chart should be made to show the routine duties of each department.

Such charts, supplying, as they do, complete working schedules for the routine of each department, soon reduce the time taken by routine tasks, which is of no little importance in the conduct of a well regulated department. They fill a place in office routine analogous to that of the working plan in the shop. The same idea can be carried out, and will prove equally valuable, even in an office where the bookkeeper does all of the work.

CHARTING SALARY AND WAGE DISTRIBUTION

22. We have seen how authorities, responsibilities and even routine duties are most graphically represented by means of charts—the working plans of the recording divisions of the business. For[39] purposes of record, the distribution of the expenditures for salaries and wages of those who make up our organization is of equal importance to the definition of the authorities and duties.

If the accounts are to be of value they must be correct, and they cannot be correct unless every item is charged to the proper account. The value of correct accounts is recognized. They do more than show what we have received or the expenditures for a specific purpose during a stated period; they show when and why an expense is increased or decreased. With such information to point the way to economies in the future, instead of records that show us merely the amount of an expense already incurred, accounting takes its rightful place as one of the most important functions of a business enterprise.

Probably more businesses have failed owing to the lack of proper accounting methods than from any one other cause. Many a business has been rejuvenated—turned from failure to success—by the introduction of a system of accounts that truthfully portrays its activities. Few business failures are the result of a failure to buy goods at right prices, or to establish selling prices that show a profit. The more usual cause is found in leaks in the expense account. Any method that locates the leaks places us in position to stop them.

The chief value of accounting records lies in the opportunity afforded for comparison. The fact that a certain expense amounted to $900.00 last month furnishes no information of special value; but when compared with the amount expended for the same purpose two, three and four months ago (if these expenses are analyzed and compared with production or sales or whatever factor would affect the amount) the figures assume an important significance. But if expenditures are erroneously applied, if an amount has crept into an expense account that does not belong there, the comparison had better not have been made. Thus is seen the necessity of an absolutely accurate distribution.

Here the chart—the working plan—is again applied to excellent advantage. The chart, Fig. 7, applied to salary and wage distribution, shows to which of the two principal divisions each item should be charged. This is the important question—to properly apply expenses to the commercial and manufacturing branches. Subdivisions of such a chart segregating expenses of each division are easily made.

The application of the items from which lines lead only to the commercial or manufacturing branch is readily understood. Between the two are several items from which lines lead to both branches, indicating that the expense is to be divided. This division should be given close study. Care must be used that too large a part of any item is not applied to either branch. The salary of the general manager, and usually the comptroller, will be equally divided. The duties of the chief accountant, chief stenographer and stenographers being chiefly in connection with the commercial branch, only a small portion of their salaries is charged to manufacturing. Shipping clerk and packers' salaries are charged to either one or the other branch, depending upon the nature of the enterprise. In a manufacturing enterprise where all goods are delivered to stock rooms ready for shipment, packing and shipping is a sales expense and is charged to the commercial branch; in a plant building heavy machinery that must be shipped from the assembling floor, this expense is usually charged to manufacturing.

EXPENSE DISTRIBUTION CHART

23. To present a graphic record of expense distribution, the chart, Fig. 8, is used. This chart separates commercial and manufacturing expense, showing amounts, while Fig. 7 shows to which branch each item belongs.

This chart subdivides commercial expense into executive, accounting, office, sales, and credits and collections, showing totals for each and for the entire commercial branch. Manufacturing expense is subdivided into executive, accounting, purchasing, engineering, and shops and equipment.

A comparison of these statements from month to month will show just what every item is and indicate the slightest increase in any class of expense. Similar charts can be readily prepared for any business, segregating expenditures of each branch, division, or department.

The distribution will naturally vary in different businesses and, before this chart can be prepared, the exact distribution must be determined. In this chart, packing and shipping is included as a commercial expense, while, as stated previously, in some businesses it would be a manufacturing expense. All such questions must be decided before the chart is prepared.

Fig. 7. This Shows How Salaries and Wages are Apportioned to the Two Principal Divisions of a Business

Fig. 8. This Chart of Expense Distribution Shows the Amount of Executive and Administrative Salaries, and Expense of Every Class, and Their Correct Apportionment

EFFECT OF PHYSICAL ARRANGEMENT

24. However efficient the personal organization, satisfactory results can be obtained only under proper environment. It is not merely a question of pleasant surroundings for employes, but a financial proposition; not a reform or a fad, but a money-making plan that governs the engineer in laying out a plant.

This is not to be a discussion of welfare work, about which much has been published. Our purpose is to point out the business economy of a proper physical arrangement of office, store or factory as against the wasteful methods of a systemless grouping of men and machinery.

The question of physical environment is a practical one that has been solved by many enterprising concerns, and the subject is deserving of careful study by the student of business organization. While some hard-headed business men may regard the question of minor importance, it is significant that the largest and most successful enterprises, financially, are those in which employes have been supplied with the most comforts, surrounded with approved safeguards, and aided in their work by the latest appliances of proved worth.

There is an old axiom to the effect that even a good workman cannot be expected to do good work with poor tools. It is equally true that he cannot be expected to do good work in either unsanitary or inconveniently arranged shops and offices.

25. Factory Plans. The planning of a manufacturing plant is a question for the engineer, rather than the accountant or business organizer, but a few general remarks on the subject will not be out of place in this paper.

It may be stated as a fundamental principle that the factory should be planned to facilitate the movement of raw material from one department to another. In the ideal factory, storage for raw material will be provided where it can be economically received and easily procured when needed in the factory. It should, if possible, be close to the department in which the material is subjected to the first operation.

The shops themselves should be arranged to facilitate the movement of partly completed parts from one department or shop to another. To illustrate, a foundry should be so located that castings can be taken direct to the machine shop, or smith shop, not through another shop or in a round-about way.

Likewise, the machine shop, if the process be continuous, should be located next to the assembling department. Or, if a "parts" storeroom is maintained, it should be located between the machine shop and assembling department. Storage for completed goods should be adjacent to the assembling department, and convenient to the shipping room or platform.

The chart, Fig. 9, shows a typical layout of a manufacturing plant operating both a foundry and wood shop. Naturally the foundry and wood shop are as widely separated as possible. Storage of foundry materials is provided for just outside of the foundry, while lumber is convenient to the wood shop.

The arrows indicate the movement of raw materials through the shops to the finished goods storeroom, and from thence to the shipping platform. If these lines are traced it will be seen that at no point is the material twice moved over the same ground. Each move takes it to the next operation and one step nearer completion. Where materials and parts enter a shop at two or more points, the lines are merged, showing that these materials leave that shop as one piece, part, or finished article. A feature underlying the whole plan is economy in the movement of work in process. All work moves through a shop, not back and forth in the shop.

The ideal conditions do not always exist, neither can they be brought about in every case. Many plants, built in the past, have been planned without due regard for these matters; their importance was not appreciated and the buildings are so located that it is impossible to secure entirely satisfactory results. However, if present conditions are studied carefully, many improvements can be brought about at slight expense. While, as we have intimated, this is a problem for engineers, a number of cases might be cited where the accountant, called in to systematize the accounting methods of a manufacturing business, has suggested physical changes in the shops that have resulted in marked reductions in costs.

26. Planning the Office. The average office is arranged in a very haphazard way. Departments are located with little regard for their departmental relations; desks are placed where they fit best rather than according to any preconceived plan.

Fig. 9. Layout of a Typical Manufacturing Plant