Title: Accounting theory and practice, Volume 1 (of 3)

a textbook for colleges and schools of business administration

Author: Roy B. Kester

Release date: March 24, 2023 [eBook #70367]

Language: English

Original publication: United States: Ronald Press, 1922

Other information and formats: www.gutenberg.org/ebooks/70367

Credits: Richard Tonsing and the Online Distributed Proofreading Team at https://www.pgdp.net (This file was produced from images generously made available by The Internet Archive)

A TEXT-BOOK FOR COLLEGES AND

SCHOOLS OF BUSINESS ADMINISTRATION

BY

ROY B. KESTER, Ph.D.

CERTIFIED PUBLIC ACCOUNTANT;

PROFESSOR OF ACCOUNTING,

SCHOOL OF BUSINESS,COLUMBIA UNIVERSITY

VOLUME I

(FIRST YEAR)

SECOND EDITION

Third Printing

NEW YORK

THE RONALD PRESS COMPANY

1922

Copyright, 1917, by

The Ronald Press Company

Copyright, 1922, by

The Ronald Press Company

All Rights Reserved

To My Father and Mother

An Appreciation of Their Steadfast

Interest in My Work

[Pg v]

The basic soundness of the method of instruction in Accounting developed in this book has received substantial demonstration throughout five years of test. The Introduction to the first edition contained the following statement regarding the development of the subject:

“The method of approach as given in this volume is perhaps not orthodox but it has seemed that the student, given an understanding of the purpose which the accounting records are to serve, will be able to make that record with real intelligence instead of by rule-of-thumb. Accordingly, the balance sheet and the profit and loss statement are presented first, as the goal towards which all record-keeping looks. The student is taught to analyze business facts and conditions from the very beginning. He is then led, step by step, through the use of non-technical terms, into the ledger, where he sees the way in which the data which he has been using are summarized. The books of original entry are next explained, and the method by which the information is classified as it is brought onto the books. Finally, the business papers and documents which constitute the source of all entries are described.”

To quote again from the original Introduction: “The subject is developed in such a way that the student knowing something of bookkeeping has little or no advantage over the one without such knowledge. This book has been written for the use of students in our colleges and universities desiring a first course in accounting. It gives the scope of the work in accounting offered in the first year of the School of Business of Columbia University.”

The method then advocated and used in a few institutions has become quite generally accepted. It has justified itself by [Pg vi] the ease and extent to which students without any previous training in accounting have grasped the essentials of the subject. Experience with the book in the classroom, however, and changing ideas with regard to manner of presentation and sequence of material, have shown as desirable a rearrangement of some parts and an addition of new material in places. Accordingly, a systematic revision has been made.

The arrangement of the subject matter of the first portion of the book has been altered but slightly. The use and function of the balance sheet and profit and loss statement have been somewhat amplified. The working sheet has been introduced earlier than in the first edition to afford an easy summary of the period’s results. It should later on be made a part of the regular work of summarization. The controlling account is also explained earlier so as to afford more practice in its use. The accounting features of the partnership and of the corporation are given continuous treatment. Here a new chapter has been added, which discusses certain features of the corporation not treated in the original book such as the issue and sale of treasury stock and of bonds, bond interest as related to premium and discount, sinking fund, sinking fund reserve, redemption of bonds, etc.

The material presented in the last quarter of the book deals with the interrelations of accounting, financial management, buying, and marketing. Thus the chapters dealing with the handling of cash, notes receivable and payable, cash discounts, and balance sheet valuation, treat of the relations between accounting and financial management. Several chapters at the end treat of some special methods of accounting practice and of the basic principles of single entry. In this portion of the book new chapters on balance sheet valuation and on buying have been added.

Entirely new problem material has been furnished, carefully graded and related so far as possible to the subject matter of the chapters of the text. For the convenience of the student this material is separated from the text, and grouped in three appendices. A few of the problems [Pg vii] have been drawn from the examinations of various state boards and the regents of the University of the State of New York, and from other miscellaneous sources, to all of which acknowledgment is due. The author is indebted to Mr. George B. Kelley for assistance in building up a large part of the practice material. It need hardly be said that a fundamentally sound knowledge of accounting cannot be gained without ample practice work. Theory can never be sure of itself until put to the test of practice.

The author desires to acknowledge again his debt to the many friends whose counsel and aid counted so largely in the first writing of this book. In the revision he finds himself still further indebted to many instructors in all sections of the country for criticism and suggestion. He desires especially to express his appreciation of the active co-operation of his associates on the Columbia staff of instructors in First Year Accounting, in particular Miss Nina Miller and Messrs. Ralph T. Bickell and E. Gaylord Davis. In the actual work of revision Messrs. Eskholme Wade, John Jaffee, and Raymond Gatchell have given valuable assistance. [Pg viii]

Columbia University,

New York City,

July 22, 1922

[Pg ix]

| CHAPTER | PAGE | |

| I | Basic Relationships—Proprietorship | 1 |

| II | Assets, Liabilities, and Capital | 11 |

| III | The Balance Sheet | 22 |

| IV | The Comparative Balance Sheet | 32 |

| V | The Economic or Profit and Loss Elements of a Business | 38 |

| VI | The Profit and Loss Summary | 44 |

| VII | Interrelation Between the Economic and the Financial | |

| Elements of a Business, and Some Inter-Ratios | 57 | |

| VIII | The Account | 67 |

| IX | The Account (Continued) | 72 |

| X | The Philosophy of Debit and Credit | 78 |

| XI | Debit and Credit as Applied to Asset and Liability Accounts | 85 |

| XII | Debit and Credit as Applied to Proprietorship Accounts | 91 |

| XIII | Debit and Credit as Applied to Mixed Accounts | 97 |

| XIV | Periodic Work on the Ledger | 106 |

| XV | Periodic Adjustments and Summarization | 115 |

| XVI | Sources of Data for the Ledger | 132 |

| XVII | The Subdivision of the Journal | 136 |

| XVIII | The Purchase and Sales Journals | 139 |

| XIX | The Cash Journals | 147 |

| XX | The Modern Journal | 162 |

| XXI | Business Papers—Negotiable Instruments | 173 |

| XXII | Business Papers—The Goods Invoice and Bill of Lading | 185 |

| XXIII | Banks and Their Methods | 192 |

| XXIV | Methods of Posting | 199 |

| XXV | The Trial Balance and Methods of Locating Errors | 204 [Pg x] |

| XXVI | The Classification of Accounts | 213 |

| XXVII | The Work Sheet and Summary Statements | 221 |

| XXVIII | Adjusting and Closing the Books | 237 |

| XXIX | Types of Accounting Records and Their Development | 251 |

| XXX | Controlling Accounts | 264 |

| XXXI | Handling Controlling Accounts | 272 |

| XXXII | Partnership from a Business Viewpoint | 284 |

| XXXIII | Partnership from the Accounting Viewpoint | 290 |

| XXXIV | Capitalization of the Partnership | 297 |

| XXXV | Other Partnership Problems | 305 |

| XXXVI | Partnership Profits | 313 |

| XXXVII | Partnership Dissolution | 321 |

| XXXVIII | The Corporation | 330 |

| XXXIX | Opening the Corporation Books | 338 |

| XL | Current and Closing Entries for the Corporation | 351 |

| XLI | Handling the Cash | 366 |

| XLII | Notes Receivable and Payable | 376 |

| XLIII | Problems Encountered in Recording Notes Receivable and Payable | 384 |

| XLIV | Discounts | 392 |

| XLV | Balance Sheet Valuation | 403 |

| XLVI | Buying and Stock Control | 420 |

| XLVII | Sales | 433 |

| XLVIII | Consignments | 447 |

| XLIX | Adventure Sales | 460 |

| L | Accounts Current | 468 |

| LI | Balancing Methods | 477 |

| LII | Some Application of Interest and Proportion | 485 |

| LIII | Single or Simple Entry | 495 |

| LIV | Illustration of Single Entry | 504 |

| Appendix | A—Practice Work for Student—First Half-Year | 513 |

| B—Practice Work for Student—Second Half-year | 553 | |

| C—Miscellaneous Problems for Supplementary Work | 597 | |

[Pg xi]

| FORM | PAGE | |

| 1. | Form of Ledger Accounts | 70 |

| 2. | Chart of Accounts | 75 |

| 3. | Accounts Balanced and Ruled | 109 |

| 4. | Transfer of Accounts to a New Page | 112 |

| 5. | Personal and Notes Payable Accounts | 113 |

| 6. | Standard Form of Journal | 135 |

| 7. | Purchase Journal | 142 |

| 8. | Modern Type of Purchase Journal | 142 |

| 9. | Departmental Purchase Journal | 144 |

| 10. | Cash Book (Cash Receipts Journal) | 148 |

| 11. | Cash Book (Disbursements Journal) | 149 |

| 12. | Columnar Cash Book—Debit Side | 158 |

| 13. | Columnar Cash Book—Credit Side | 159 |

| 14. | Divided Column Journal | 164 |

| 15. | Opening Entries on Books | 166 |

| 16. | A Promissory Note | 175 |

| 17. | A Draft | 175 |

| 18. | A Bank Draft | 180 |

| 19. | Forms of Checks | 182 |

| 20. | Monthly Statement of Account | 191 |

| 21. | Bank Deposit Ticket | 193 |

| 22. | Cross-indexing in Posting | 202 |

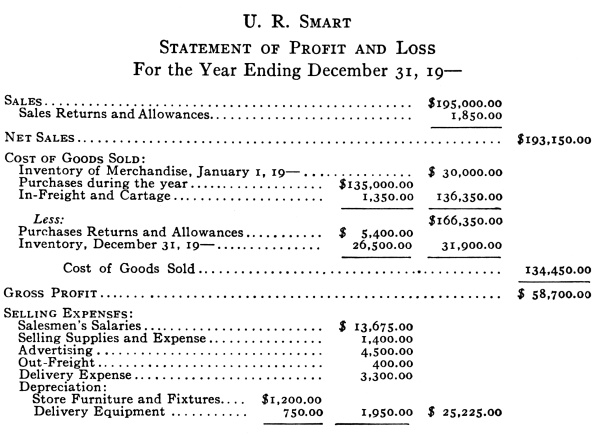

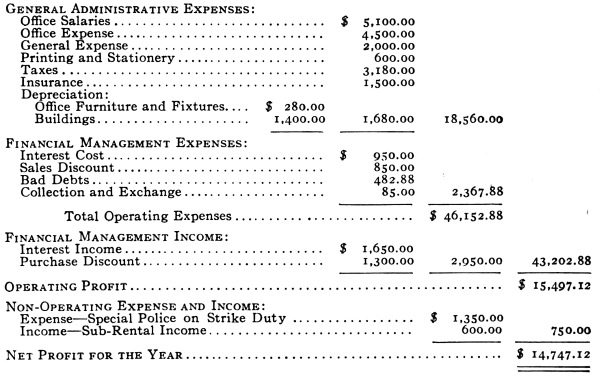

| 23. | Work Sheet | 226-227 |

| 24. | Balance Sheet—Report Form | 232 |

| 25. | Balance Sheet—Account Form | 233 |

| 26. | Statement of Profit and Loss—Report Form | 234 |

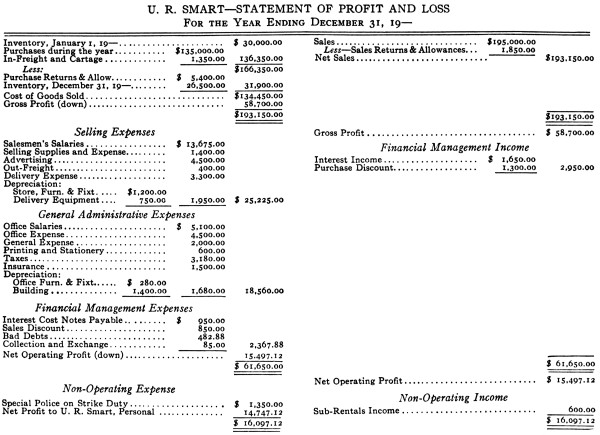

| 27. | Statement of Profit and Loss—Account Form | 235 |

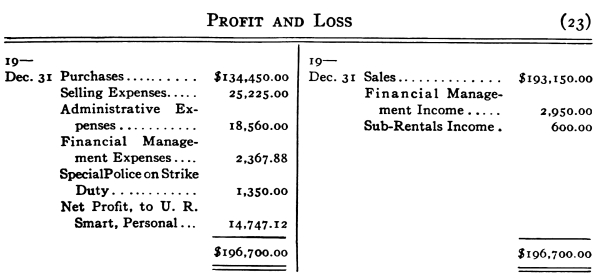

| 28. | Profit and Loss Account in Ledger | 249 |

| 29. | Standard Ledger—Divided Column | 258 |

| 30. | Standard Ledger—Center Column | 258 |

| 31. | Balance Ledger Rulings | 259 |

| 32. | Balance Ledger Rulings | 259 |

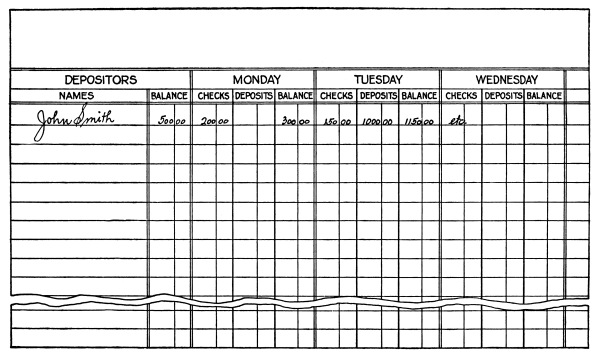

| 33. | Boston Ledger Sometimes Used for Depositors | 262 |

| 34. | General Journal | 279 |

| 35. | Sales Journal Summary | 279 |

| 36. | General Journal Summary | 281 |

| 37. | Cash Book Summary Book—Receipts Side | 282 |

| 38. | Cash Books Summary Book—Disbursements Side | 282 |

| 39. | Petty Cash Book | 369 |

| 40. | Weekly Statement of Receipts and Disbursements | 375 |

| 41. | Notes Receivable Journal | 380 |

| 42. | Discount Columns Used for Cash Balance | 400 |

| 43. | Stock Control Card | 430 |

| 44. | Account Sales | 451 |

| 45. | Form of Adjusted Account Current | 470 |

| 46. | Account Marked for Analysis | 478 |

| 47. | Ledger Analysis Sheet | 480 |

[Pg 1]

Accounting—Theory and Practice

Records and Their Functions.—As far back as our knowledge reaches, records of some sort have been kept and used and they have frequently formed the basis on which our knowledge rests. In a broad sense a record may be defined as a written memorial, a register or history of events, a testimony. Even though the desire to make and hand on to the future a record of achievement is a deep-seated characteristic, record-making has seldom been an end in itself. Knowledge of what has been done has always been a starting point and a guide for future achievement. The longhand or narrative record is indispensable in some fields of knowledge; the shorthand or statistical record is equally necessary in others. The statistical method and accounting are, without question, most potent agencies for the advancement of human knowledge and for the control of human relationships. They provide the basis in fact on which judgments must largely rest. This book, therefore, may begin by sketching the relation of accounting to some of the larger fields of human endeavor—the economic organization of society and the law—to point out its place in the business unit and briefly state the basic function it performs therein.

The Business Unit.—To carry on its various activities, economic [Pg 2] society has organized itself into numberless separate units or business organizations. These units are the means through which society operates, their ultimate purpose being the easy and efficient satisfaction of human economic wants. Individual business units, conducted as they are by members of society, are under the broad general supervision of society as a whole. This is evidenced everywhere by the laws, licenses, and regulations by which society attempts to regulate the activities of the individual for the larger interest of society as a whole. As business is conducted in most parts of the world, it is highly individualized rather than communized. There is a growing tendency, however, for society to exercise a larger control and supervision over all types of individual activity, particularly with a view to conserving the welfare of its members. The business unit is thus the medium through which society works to satisfy its economic wants.

Internal Organization of the Business Unit.—Society early found that only by means of a highly specialized division of its activities was it possible to satisfy without waste its rapidly increasing economic wants. Individual business units are thus organized for the purpose of carrying on some one or more of these greatly subdivided activities. Within itself the business unit is organized into departments or divisions for the efficient and thrifty handling of its work. The two large divisions in any business undertaking have to do with what the economist calls the production and exchange of wealth, that is, commodities, services, and so forth. In carrying on these activities of production and exchange it has usually been found desirable to segregate into separate departments certain major functions which are common both to production and to exchange. What the major departments may be depends very largely upon the size of the business unit, its relative complexity of organization, and to some extent on the individual ideas of its managers. Throughout the business world one notes, however, a quite general departmentization under the following heads: [Pg 3]

There are two main activities under the control of the finance division of a business: (a) the problem of original investment, including that of location and acquisition of a plant suitable for the conduct of a contemplated business; and (b) the problem of operating finance, that is, of providing the business with a fund of working capital for its efficient operation. The financing of purchases, sales, credits, operating expenses, and so forth, comprises a large part of the work of finance of an operating or going concern.

In the second of the major departments, that of procurement or production, one finds these activities: (a) the purchasing of the stock-in-trade to be dealt in, if the concern is a trading business; or (b) the manufacture of the stock-in-trade, if the concern is a manufacturing business.

In the department of marketing or distribution, the following activities center: (a) those having for their purpose the creation of a market or demand for the commodity dealt in—the sales organization, the advertising activities, and so forth; (b) the actual selling of the commodity; and (c) the transportation and delivery of the product.

In the personnel department are included the human relations between employer and employee. The hiring and training of the employee, his classification and rating, his welfare and promotion, are the major activities here.

The function of the department of general administration is in the main that of supervision and management of the business as a whole. The general manager must have a view of all of the activities of the business. He must see that the various departments through which its activities are carried on are properly correlated, that it is so [Pg 4] organized that its departments function smoothly and efficiently in the performance of their several duties. A consideration of the means employed by the general manager for the proper performance of his duty indicates the place of accounting in the business unit.

Place of Accounting in Business.—In a small business where the owner and manager is in close and intimate contact with these several departments, or perhaps where he focuses all of them within himself, he has no need of special means of keeping himself informed concerning the activities of his assistants, nor does he require an elaborate system of records to indicate the condition and state of the business at any time. In large businesses, however, where the volume and complexity of the commercial activities make it impossible for the executive, on whom rest the responsibilities for the successful conduct of the business, to have an intimate personal knowledge of all phases of the business, it is very necessary that some means be employed for supplying him with this vital information. Two types of information are necessary to him: (1) information about the business unit itself, its activities and condition; and (2) information about general economic conditions in the country, and particularly about other businesses in the same line of activity as his own. It is the function of accounting to supply information of the first type; it is the chief purpose of statistics to supply information of the second type. The accounting department, therefore, deals largely with the internal activities of the business, while the statistical department provides knowledge of the external relations of the business. A proper control and management of business affairs cannot be exercised without the information supplied by both departments. In the accomplishment of its function to supply the internal information, the accounting department reaches out into all of the main departments indicated above for data from which to make its record of the various activities of the business unit. [Pg 5]

Purpose of Accounts.—Accounts record the business history of a concern. Their main purpose is to secure information concerning the results of business activity and endeavor. The record required for this purpose can be condensed and made very brief, although the full history of every business comprises a multitude of transactions with a great mass of details. The whole scheme and method of account-keeping is designed chiefly to collect the detail and use it mainly for building up a summary which shall give in rapid review the entire record for the fiscal period.

Account-keeping is to the bookkeeper what shorthand is to the stenographer—an abbreviated method of making the record. The uses to which the records are put, however, differ radically. Stenography abbreviates the writing of the spoken word with a view to its transcription into longhand; accounting records business transactions in abbreviated form with a view to summarizing them further so as to secure a bird’s-eye view of the operations of the business as a whole and to use it in the formulation of administrative judgments and policies.

In a large business there are executive duties within each of the five main departments. Accounting must supply the information on which each departmental executive will base his judgments and policies. The student will see, therefore, that the accounting department brings together a record of the activities of each of the main departments of a business. He will see, too, how the final output or product of the accounting department must be a summarization and interpretation of these departmental activities in order to provide a basis for the various executives on which to formulate their judgments and business policies. Accounting is, therefore, a handmaiden of the executives in the conduct and management of the business. It is the purpose of this volume to develop the technique of the bookkeeping and accounting record and to indicate some of its uses in the management of business. [Pg 6]

Relation of Accountancy to Economics.—Economics is sometimes defined as the science of wealth, by which is meant a body of classified knowledge relating to wealth in the aggregate. Under the present-day political and social system, the ownership of wealth is very largely private. Furthermore, the division of labor, as industry is now organized, has been carried to a very high degree. Because of these facts the present elaborate organizations for producing wealth have given rise to an urgent need for some effective means of keeping record of their activities.

The effort of every individual engaged in industry is to increase wealth. He labors to extract the raw materials from nature, to shape and mould them so as to supply the wants of his fellowmen. He then distributes them by means of markets and exchanges so as to secure the greatest possible returns for his effort. As competition becomes keener and the margin of return per unit of product becomes smaller, he has to increase his volume of business to secure the same amount of profit as when he did a lesser volume of business.

To produce goods it is necessary to use the saved wealth of former periods to pay the expenses of materials, labor, management, etc., of the present period. One must consume wealth to produce wealth. After his product is made, he must seek the best market for its exchange or sale. This necessitates the use of a complex system of transportation and communication. Finally, during the whole process of production and exchange the estimated returns from the article must be distributed among the several parties engaged in their creation. To make this distribution on the basis of estimated returns, gives rise to the need—the absolute necessity—of an accurate record of the costs of the activities and processes all along the line. The record, then, of the value of the rights and properties of the various parties to the production and distribution of wealth, as society is now organized for its economic well being, is the special field assigned to Accountancy as related to Economics. [Pg 7]

Relation of Accountancy to Law.—The determination of the rights of the several parties to the creation, exchange, and ultimate consumption of a product is the field of Law, more particularly Business Law. The determination by means of its records of the value and extent of these rights is the province of Accountancy as related to Law. Accountancy is thus seen to be the handmaiden of both Economics and Law. None of them can progress far without the help of the other two. All being related to, and arising out of manifold human endeavors, their progress and development is dependent upon, and limited only by, the progress of these endeavors.

The Fundamental Problem of Accountancy.—The aim of all private businesses being the increase of wealth, the first problem of accountancy is to determine how much wealth is invested in a given enterprise and what ownership or proprietorship exists at given periods, so that by comparison the increases and decreases in the proprietorship may be known. When accurate information is obtained, an intelligent plan of action can be adopted to remedy such ills of the business as are shown and to increase any profitable line of activity. Accordingly, proprietorship and its changing values are the basic problems of accountancy as well as of business.

Definition of Terms.—Before proceeding to a definition or determination of proprietorship, it is necessary to understand what is meant by the terms “assets” and “liabilities.” The root idea of the word “assets” is “sufficiency.” Specifically, assets are the “entire property of all sorts, of a person, association, or corporation applicable or subject to the payment of debts.” Similarly, the liabilities of a person, firm, or corporation are his or its pecuniary obligations or debts. Proprietorship is the difference between the value of the assets and the amount of the liabilities, and is defined and measured by the equation:

Assets - Liabilities = Proprietorship

[Pg 8] This proprietorship equation is a basic formula. It is also written:

Assets = Liabilities + Proprietorship

It will thus be seen that proprietorship represents the equity of the owners of an enterprise in its assets. The assets are first applied in paying the claims of creditors of the business, and whatever of them remains belongs to the owners of the business.

Development of the Proprietorship Equation—The Balance Sheet.—To indicate the basis of the standard form of the proprietorship equation, several illustrations will be given. The equation is in its simplest form when it indicates proprietorship in a new business immediately after the owner has invested cash to provide the business with capital. For example, assume that on January 1, 19—, James T. Runyon starts business by investing $5,000 cash capital in the enterprise.

Here the proprietorship equation is:

Assets (cash $5,000) = Proprietorship ($5,000)

As yet there are no liabilities. However, in order to carry on his business, Runyon must purchase a stock of merchandise and equipment for his store. Accordingly, he purchases store furniture and fixtures from Lowell Brothers for $500, of which he pays $250 in cash, and owes the balance. He also buys a stock of groceries for $2,500 from Reid Murdock & Co. on 10 days’ time. He now has more assets than the original $5,000 cash, but he has become indebted for the additional amount, so that the amount of his proprietorship has not changed—as is shown by the following equation, somewhat more complex than the first:

| Assets | - Liabilities | = Proprietorship | ||

| Cash | $4,750 | Lowell Bros. | ||

| Furniture | 500 | Claim | $ 250 | |

| Merchandise | 2,500 | Reid Murdock | ||

| Claim | 2,500 | |||

| $7,750 | - | $2,750 | =$5,000 | |

[Pg 9] Runyon now begins operations and after six months finds that his activities have comprised the purchase of delivery equipment for $300 cash; sale of goods amounting to $6,000; the payment of $1,000 cash for rent, clerk hire, and advertising; and sundry purchases of stock-in-trade and other items as needed. As a result he now has $1,000 cash on hand; customers owe him $3,000; his stock of goods still on hand is worth $2,100; he owes creditors $1,000 for goods bought and his clerks $50 for services rendered.

It is readily seen that as the number of assets and liabilities increases, the method of showing them that was used above becomes awkward and cumbersome; therefore, still using the equation, we make the following vertical tabulation to determine and show proprietorship:

| Assets | ||

| Cash | $1,000.00 | |

| Customers | 3,000.00 | |

| Merchandise | 2,100.00 | |

| Furniture | 500.00 | |

| Delivery Equipment | 300.00 | |

| Total Assets | $6,900.00 | |

| Liabilities | ||

| Creditors for Merchandise | $1,000.00 | |

| Clerks for Services | 50.00 | |

| Total Liabilities | 1,050.00 | |

| Proprietorship | ||

| Capital | $5,850.00 | |

This method of expressing the proprietorship equation is called a “Balance Sheet,” or “Financial Statement.”

Further analysis of the above information discloses the amount of Runyon’s purchases and of his payments to creditors. Taking the transactions involving cash, we find that he had $5,000 to start with and received $3,000 from sales, or $8,000 in all. He bought furniture and delivery equipment for $800, and paid expenses of $1,000, in all [Pg 10] $1,800. There is therefore a balance of $6,200 to be accounted for. $1,000 cash is still on hand, so that he must have paid creditors $5,200. Since he still owes creditors $1,000 for goods bought, his purchases must have been in all $6,200.

The ability to make accounting statements and to analyze accounting data for various purposes constitutes a very important part of the equipment of the accountant.

[Pg 11]

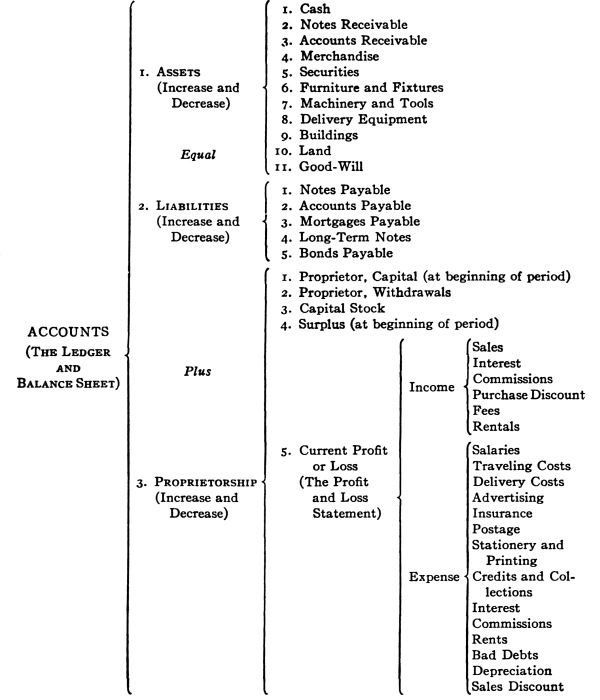

Before discussing the form and content of the balance sheet and some of its major uses, the chief classes of assets, liabilities, and proprietorship or capital will be explained so that the student will have an intelligent notion of what is meant by each asset, liability, and capital item.

Kinds of Assets.—Accounting terms are not wholly standard. An account title is often used in one business to include items not mentioned under that title in another business. One finds also terms and titles peculiar to particular businesses. However, there is a tendency towards a standardization of the terms used in balance sheets. It is the purpose here to present and explain those which are common to practically all businesses. These include the asset titles Cash, Notes Receivable, Accounts Receivable, Merchandise, Investments, Deferred Charges or Expense Assets, Furniture and Fixtures, Delivery Equipment, Buildings, and Land.

Cash. Cash includes all kinds of money and usually whatever serves as a medium of exchange, which is in the possession or control of the business—deposits in banks, moneys in the safe and cash drawers, and sometimes funds in the possession of agents. Checks received in the regular course of business and not yet deposited in the bank are usually classified as cash.

Notes Receivable. The formal promises to pay, made by others for debts owed the business, are classified under the general title Notes Receivable. Time drafts drawn on the debtors of [Pg 12] the business and accepted by them may be included under this title, although they are sometimes shown under a separate title, such as Acceptances Receivable. This is particularly true when the acceptances are trade acceptances. It will be seen later that the promissory note has a somewhat different legal status from the open account claim against a debtor, and should therefore be classified under such title as will indicate the exact nature of the item.

Accounts Receivable. These usually represent the claims of the business against its trade customers for goods sold on open account and not paid for. The term is, however, broader than this, being sometimes used—although the practice is to be deplored—to include all claims against debtors except those which are in the form of notes.

Merchandise. This asset represents the stock-in-trade in which the business deals. It is of course a sort of revolving asset, that is, merchandise is purchased and sold continuously, so that the stock-in-trade is constantly being turned over. The rate of turnover is very important, as will later be seen.

Investments. This asset represents the stocks and bonds of other companies, municipalities, school districts, and so forth, owned by the business. As a usual thing there are seasons of the year when the cash funds of a business are built up and lie idle in the bank unless they are invested in securities of some sort. These securities can be reconverted into cash when the business requires a larger fund of cash.

Deferred Charges. Certain types of expenditure are necessary in every business to secure operating supplies. Fuel must be purchased for heating and power purposes; brooms, oil, waste, and other similar supplies are needed for cleaning and maintaining the business plant; stationery, stamps, wrapping paper, twine, cartons, packing materials, and so forth must always be on hand; insurance policies giving protection against fire are usually purchased [Pg 13] for from one to three years and so are seldom completely used up at any given date. All items of this sort, necessary for the operation of the business but not dealt in as stock-in-trade, are called “expense assets.” The portions of these assets on hand at a given time, the use of which will be deferred to a later period, are classified as “deferred charges.”

Furniture and Fixtures. A business plant must be equipped with furniture and fixtures suitable for the display of the stock-in-trade, for the accommodation of customers, for the care and protection of the necessary records of the business, for the efficient performance of duties by the employees, and for other similar purposes. Assets of this type which are not a permanent part of the business plant but are removable should the business desire to change location, are listed under the title of Furniture and Fixtures. This may be subdivided to suit conditions. Sometimes several titles—Store Furniture and Fixtures, Office Furniture and Fixtures, Factory Furniture and Fixtures, Machinery and Tools—are used.

Delivery Equipment. If a business delivers its commodities it will usually have its own delivery equipment. This may comprise horses, wagons, harness, automobile trucks, and so forth. The delivery equipment may be used for both inbound and outbound deliveries.

Buildings. All buildings owned by the business, whether used for business purposes or not, will usually be classified under the asset title Buildings. Store, office, factory, warehouses, residences owned and rented to employees—all assets of this type are to be listed here.

Land. This item represents land—city lots, plant sites, and so forth—owned in fee simple or subject to mortgage. Sometimes when a plot of land is leased for a term of years and a lump sum payment made at the beginning of the lease, the asset may be included either under the title Land, or under the broader title Land and Leaseholds. [Pg 14]

Kinds of Liabilities.—Just as with assets, there is not entire uniformity in terminology for the various classes of liabilities. The more common types of items met with are: Notes Payable, Accounts Payable, Accrued Expenses, Mortgages Payable, Bonds Payable, and so forth.

Notes Payable. These represent the formal promises to pay, signed by the business or its owners. They represent the formal claims of others, that is, creditors, against the business. Just as with notes receivable, it is sometimes desirable to make a more distinct classification of notes payable. In such cases the titles Acceptances Payable, Trade Acceptances Payable, Long-Term Notes Payable, etc., are used.

Accounts Payable. Under this title are listed the liabilities to creditors on open account, as distinguished from those formally acknowledged by a written promise to pay. These include obligations to trade creditors for merchandise, supplies, equipment, and property of almost any kind purchased for use by the business. In a broad sense an account payable includes any item for which the business is liable.

Accrued Expenses. Accrued Expenses represent usually the accumulating but unpaid claims against the business for service rendered it, as distinguished from the Accounts Payable, which usually represent purchases of an asset of one kind or another. Thus the amounts due at a given time to employees for work done since the last date of payment of their wages, salaries, or commissions, to the landowner for the rent of leased premises, to lenders for interest on moneys borrowed, are items properly to be listed under this title.

Mortgages Payable. These represent the claims of creditors against particular properties owned by the business but against which the creditors have been given a lien or preferred claim as security for the borrowed or unpaid amount. Mortgages are evidenced by a formal legal document and are usually recorded in the county clerk’s office. [Pg 15]

Bonds Payable. These are a type of long-term mortgage which is split into lots of more or less standard amount and so made available to a larger number of holders than is usually the case with the ordinary mortgage payable. This type of liability is limited almost exclusively to corporations.

The student should realize that usually the owner or owners of a business enterprise have both assets and liabilities other than those employed in the business. These personal properties and obligations of the owners are not to be taken into account when showing the proprietorship of a business unit or enterprise. They are to be considered only in showing the total proprietorship of any individual owner, when of course all of his properties, both inside and outside of the business, must be listed.

Kinds of Proprietorship.—Proprietorship, called also Net Worth, is shown under such titles as Capital, Investment, Capital Stock, Surplus, Undivided Profits, Reserves, and so forth. The title used depends largely on the type of organization under which the business is operated.

Capital. Under this title is shown the amount of the investment of each owner in a single proprietorship or partnership business. To show each owner’s share in the ownership the title Capital is preceded by his name. Illustration of this is given on pages 19 and 20.

Investment. This title usually is synonymous with capital. Sometimes it is used to indicate the amount of original investment in the business as distinguished from the present investment.

Capital Stock. Under this title is indicated the sum total of the portions of net worth owned by the shareholders as evidenced by stock certificates and subject to their individual control. On page 20 is given an explanation of the way in which the proprietorship or net worth of a corporation may be composed of two (or more) parts: (1) the capital paid in by the owners; and (2) [Pg 16] the capital, representing profits made but not distributed to the owners. While capital stock usually represents the capital contributed by the owners, it sometimes arises from other sources, such as the distribution of a stock dividend; but the portion of the net worth owned and controlled individually by the owners is the capital stock.

Surplus. In a corporation this represents the second portion of the net worth, as indicated in the preceding section. Surplus is sometimes defined as the excess of the net worth over the capital stock. In other words, it is the difference between the assets and the sum of the liabilities and the capital stock.

Undivided Profits. This is a term used chiefly in financial institutions to indicate the portion of the net profits concerning the disposal of which no action has been taken.

Reserves. Under this title are included whatever portions of the surplus are set aside or reserved for specific purposes.

Where Surplus, Undivided Profits, and Reserves appear as parts of Net Worth, they together represent the difference between Net Worth and Capital Stock. The reason for the careful segregation of these items from the Capital Stock is given in the explanation of the corporate form of organization, on page 20.

Types of Business Organization.—Before proceeding with a discussion of proprietorship as it appears on the balance sheet, the three general types of business organization will be treated briefly, because the manner of indicating proprietorship is dependent to a certain extent on the type of organization. These types are: (1) the single or sole proprietorship, (2) the partnership, and (3) the corporation.

The Single Proprietorship.—The simplest form of business enterprise is that conducted by a single proprietor. This form is well adapted to businesses where the capital necessary for efficient production is small, where the processes are simple and capable of [Pg 17] being handled by the average individual, and where the risks are slight. Very few legal obstacles are placed in the way of the individual desiring to go into business for himself, nor is a great deal required of him. In some cases registration and a license are necessary. The observance of the general laws, concerning the payment of taxes and of local regulations concerning disease and fire is all that is usually expected. Subject to the general restrictions which ordinary business acumen and foresight impose, one can enter practically any field of enterprise, as a single proprietor, have entire freedom and privacy in the conduct of his business, and share with none the results of his endeavor.

On the other hand, these conditions oftentimes prove to be decided disadvantages. As industry is at present organized, many fields of activity demanding large capital and many kinds of technical knowledge, are closed to the single proprietor. Freedom of action carries with it sole responsibility, and oftentimes the counsel and advice of others would prevent the disasters which sometimes overtake the single owner of a business.

The Partnership.—A partnership is “a contract of two or more legally competent persons to combine their money, property, skill, and labor, or some or all of them, for the prosecution of some lawful business and to divide the profits and bear the losses in certain proportions.” There are different kinds of partnerships, as will later be shown, but the essence of each from the point of view of a working organization is mutual agency, each partner being the agent of the others, and, within the limitations of the partnership agreement, capable of acting as a principal for the firm. The partnership is subject to practically as few restrictions as the individual. In some localities, to secure the right to sue and be sued in the firm name, it is necessary to file in a public office a brief statement of the firm name and the names of its members.

The chief advantages of the partnership are larger capital and [Pg 18] therefore access to fields closed to the individual; the combining of the business wisdom, skill, and knowledge of several individuals; the subdivision of duties and therefore the opportunity for specialization. While in the view of the business community the partnership is an entity or a business unit, it is not so in the sight of the law, each member of the firm being held liable to creditors for the entire debts of the partnership as if it were his sole business. If any one member has to pay the firm debts, he has a claim against his copartners for contribution.

Some of the disadvantages of this type of organization are the possibility of friction among the partners and consequent delay of action; the extension to the firm of credit based not on the firm property but rather on the total property of the members, and the consequent liability of each partner and his entire private fortune for the debts of the firm.

It is important to note that the partnership agreement should be very carefully drawn to cover in detail the relations of the partners, their duties and their rights, particularly as to their shares in the profits or losses of the firm.

The Corporation.—The corporate type of business organization is distinguished from the other types discussed:

1. By the freedom of each owner from the personal liability for the debts of the business to any greater extent than his stock interest in the business, though frequently in financial corporations, and in a few states for all corporations, his liability is double that stated.

2. By each share of ownership being evidenced by a formal document called a certificate of stock.

3. By each owner being allowed a voice in the affairs of the business only to the extent of his stock ownership therein.

4. By the necessity of securing from the proper authorities permission to do business.

5. By the necessity of complying strictly with the terms of this permit and submitting to certain requirements such as the filing of annual reports, payment of special taxes, and the like.

The owners of a corporation, or its stockholders as they are called, [Pg 19] conduct the business through a board of directors which they elect for that purpose and they review its management periodically, usually annually. In this way they exercise indirect supervision over the business. This remoteness of personal interest and supervision has been somewhat overcome by electing to the board only those largely interested in the business, and by retaining on the board those whose ability as managers has been tried and proved. The board usually hires and delegates to others the active management of affairs.

The advantages of the corporate form of organization are: (1) it limits the liability of its owners; (2) it lends itself well to accumulation of the large funds of capital necessary for the promotion of large-scale enterprises; and (3) it secures through its board of directors a convenient and effective means of centralized control and management.

Showing the Proprietorship of These Types.—The methods of showing in the balance sheet the proprietorship for these three types of organization differ somewhat. The title under which proprietorship is listed is Capital. In a single proprietorship such title is preceded by the proprietor’s name, as shown in the following illustration:

| Assets | ||

| Cash | $2,000.00 | |

| Accounts Receivable | 5,000.00 | |

| Merchandise | 3,000.00 | |

| Furniture and Fixtures | 500.00 | |

| Total Assets | $10,500.00 | |

| Liabilities | ||

| Accounts Payable | $4,450.00 | |

| Due Clerk | 50.00 | |

| Total Liabilities | 4,500.00 | |

| Proprietorship | ||

| James Runyon, Capital | $ 6,000.00 | |

[Pg 20] In a partnership the capital is not shown in one item, each partner’s interest being stated separately, thus:

| Assets | ||

| Cash | $ 2,500.00 | |

| Accounts Receivable | 10,250.00 | |

| Merchandise | 8,750.00 | |

| Furniture and Fixtures | 625.00 | |

| Total Assets | $ 22,125.00 | |

| Liabilities | ||

| Notes Payable | $ 1,660.00 | |

| Accounts Payable | 5,465.00 | |

| Total Liabilities | 7,125.00 | |

| Proprietorship | ||

| Represented by: | ||

| James Runyon, Capital | $ 8,000.00 | |

| Philip Adams, Capital | 7,000.00 | $ 15,000.00 |

In a corporation, proprietorship is shown by the aggregate of the outstanding shares of stock, which are valued at a fixed par, or cost, under the single title Capital Stock, and if the proprietorship is greater than that indicated under this title, the excess is listed separately under the title Surplus or some of the other proprietorship titles already explained. This method of showing proprietorship is prescribed by law and is an effort to inform creditors, or those who may become creditors, that the corporation has observed the legal requirement not to distribute to stockholders any of its original capital. Hence, the capital stock of the corporation must be listed separately from the other items of proprietorship. Any changes in proprietorship during the life of the corporation are taken care of under these other titles, somewhat as illustrated below. [Pg 21]

| Assets | ||

| Cash | $ 1,850.48 | |

| Notes Receivable | 1,645.65 | |

| Accounts Receivable | 15,285.35 | |

| Merchandise | 10,045.94 | |

| Supplies | 1,145.37 | |

| Furniture and Fixtures | 1,636.97 | |

| Delivery Equipment | 1,427.50 | |

| Buildings | 8,000.00 | |

| Land | 2,000.00 | |

| Total Assets | $ 43,037.26 | |

| Liabilities | ||

| Accounts Payable | $ 5,762.26 | |

| Notes Payable | 4,250.00 | |

| Salaries Due but Unpaid | 25.00 | |

| Mortgage on Land and Buildings | 3,000.00 | |

| Total Liabilities | 13,037.26 | |

| Proprietorship | ||

| Represented by: | ||

| Capital Stock | $ 25,000.00 | |

| Surplus | 5,000.00 | $ 30,000.00 |

[Pg 22]

Purpose and Use.—The balance sheet of a business is designed to show its financial condition at a given time. As previously illustrated, it marshals the assets in one list or schedule, and the liabilities in another. The difference between the totals of the two schedules gives the present or net worth of the business. In compiling a balance sheet it is not sufficient to give simply the figures of proprietorship or net worth; schedules of assets and liabilities must be drawn up to show the items making up that net worth. From the viewpoint of a prospective investor or purchaser, a banker to whom the business has applied for a loan, or a concern considering the advisability of extending it credit on a bill of goods, it makes all the difference in the world to know that with a net value of $10,000 the business has assets of $15,000 and liabilities of $5,000; or to know that its assets are $260,000 and its liabilities $250,000.

The ratio of total assets to total liabilities is almost as important information to an investor, purchaser, banker, or creditor as is the character of the assets and liabilities. If the assets are in properties for which there is not a ready market and the liabilities are claims which mature soon and will have to be met, the situation is unfavorable. If there are large values invested in easily salable assets; if there is a large balance of cash on hand after meeting current claims and providing for those which will soon mature; if other liabilities are of a more permanent nature, such as mortgages or long-time notes not requiring immediate attention—the situation may show evidence of too large a capital, or of inefficient management as [Pg 23] indicated by the failure to invest a part of the surplus cash in properties from which some return might be secured.

Form and Content.—Questions of the kind raised above are not usually capable of definite answer from the information contained on the balance sheet alone. Oftentimes information as to the volume of business done, future plans for expansion or contraction of business operations, and so forth, is needed in addition to that supplied by the balance sheet. Of immediate interest to us, however, is the information contained in the balance sheet. Here two main problems are met: that relating to the form of the balance sheet, and that concerned with the content of the balance sheet.

By form of the balance sheet is meant its physical appearance—the arrangement and classification of its items. The form is not standard. In this country there are few legal regulations governing the way in which the records of a business are to be kept or its reports are to be made. Some efforts have been made, however, to establish a more or less standard form of balance sheet and to secure the use of standard titles in the balance sheet so that wherever found those titles can be relied upon to mean one and only one thing. Because balance sheets are not always drawn up for similar purposes, such regulations should not be too inflexible. The form of any business statement or report should always have regard to the purposes it is to serve. Standardization of form is desirable within this limitation.

By content of the balance sheet is meant the items that are admitted to it and the basis of their valuation.

These two problems of the balance sheet—form and content—are fundamental and will be briefly considered here.

Titles—Main and Group.—Instead of “Balance Sheet,” other terms are used as names for the statement itself, such as “Financial Statement,” “Statement of Resources and Liabilities,” “Statement of [Pg 24] Assets and Liabilities.” Within the statement, Resources is an alternative title for Assets; and Net Worth, Present Worth, and Net Assets, for Proprietorship. For the present, use of the terminology previously employed will be continued, with the substitution, however, of the term Net Worth for Proprietorship.

The title of a statement should be full; it should include the name of the business enterprise and date, and should appear somewhat as follows:

Shongood & Goodwell

Balance Sheet

December 31, 19—

As stated, this should be followed by the schedules of Assets, Liabilities, and Net Worth. Since the statement is a formal one, due regard should be had for its general appearance, which should be neat and attractive. Further consideration will be given to some of these features in Chapters XXVI and XXVII.

Classification and Arrangement.—As indicated above, the balance sheet is used to picture the financial condition of a business at a given time. Some of the questions which arise in determining the financial condition of a business have already been mentioned. The chief use to which a balance sheet is put is the determination of the solvency of the business for purposes of getting credit extensions. By solvency is meant the ability of the business to pay its debts when due. Regardless of how great the excess of assets over liabilities is, if it is tied up in assets which cannot be used for the payment of debts, the creditors of the business will become impatient and may ask a court to take the control of the business away from its owners and place it in the hands of a representative of the court and the creditors, who will conduct the business for the purpose of converting assets into cash to a sufficient extent to pay all debts.

A balance sheet should therefore be so arranged that the condition of [Pg 25] the business, viewed from the standpoint of its ability to pay its debts, will be clearly and easily determinable. Cash is usually the only medium used for the payment of debts. In the regular course of business, debts are incurred which come due at different dates. Hence it is not necessary to have on hand at a given time cash sufficient to pay all of the debts of the business. Certain classes of debts will not wait. The sums owed employees for services must usually be paid when due. The debt to the government for taxes, to the public service company for heat, light, and power, to the landlord for rent, to the bank for money borrowed—all these debts must usually be paid immediately as they come due.

The cycle of business operation includes the purchase of merchandise, the payment of operating expenses, and the conversion of merchandise into cash through sale, either directly, as when the sale is for cash, or indirectly as when credit is extended a customer and cash is later collected from him. This cycle or turnover of merchandise recurs constantly in the management of the financial affairs of a business. It is necessary so to order the buying and selling of goods and the collection of accounts from customers that there will be on hand at all times sufficient cash to pay the expenses of operating the business and the debts contracted in the purchase of merchandise. This is the vital and fundamental problem of the business executive. In the solution of that problem it may sometimes be necessary to borrow funds from the bank. Before lending money, the banker assures himself that the business will be in a position to repay the borrowed money when due.

The balance sheet, accordingly, should be so arranged that the condition of the business as related to its ability to pay its debts will be apparent. This requires a classification or marshaling of the assets which are concerned in the trading cycle on the one side, and the liabilities which must be assumed in conducting the business during the trading cycle, on the other.

At the head of the list of assets is the item Cash, the most liquid of [Pg 26] all, as it can be used directly for the payment of debts. Following Cash come in order Notes Receivable, which, with proper indorsement, can be sold to the banker and converted into cash almost immediately; Accounts Receivable, which represent the claims against customers for merchandise sold and which are collectible within the term of credit extended to the customer; and finally, the Merchandise on Hand, which must be sold either for cash or on credit and then converted into cash by the collection of the outstanding accounts. Sometimes, also, there is included in this group the asset Investments, representing stocks and bonds of other companies which can be converted into cash by sale on a stock exchange. On such securities, and also on the notes receivable, there is usually at the date of the balance sheet some interest which has accrued and may not yet be collectible. It is customary to include the amount of this interest receivable in the same group with the assets from which it arises.

This group of assets, comprising Cash, Notes and Accounts Receivable, Merchandise, and so forth, is called the group of Current Assets. Asset items are classified as current if conversion into cash is expected within three to six months. These are the assets to which the current creditors of the business will have to look for the payment of their claims.

The claims of current creditors are usually included under the titles Notes Payable, Accounts Payable, and Accrued or Unpaid Expenses. The classification of a creditor in the current liability group is usually determined on a time basis. Thus, all debts that will have to be met within six months’ or one year’s time from the date of the balance sheet are usually classed as Current Liabilities.

The excess of current assets over current liabilities is called the working capital of the business; that is, an amount of the current assets equal to the current liabilities will have to be used for the payment of these debts, leaving the excess or difference free for use within the business. While it is not possible to determine, without considering all the circumstances in a given case, how large this [Pg 27] working capital should be, the standard rule-of-thumb is that it should equal the amount of the current liabilities. It will thus be seen that the standard ratio of current assets to current liabilities is two to one. The solvency of a given business is always judged by a comparison of the current asset group with the current liability group.

The next main group of assets is given the title Deferred Charges. The content of this item was explained on page 12. Thus, if a management has paid some of its expense bills in advance—rent for January paid during December, for example—when showing its financial condition as at the end of December it is proper and necessary, in order to make an accurate showing, that all such prepaid expenses be listed as assets; for, had the payment not been made until the service which it purchased had been used up, the asset cash would have been larger by the amount of the prepaid expenses.

Similarly, with regard to the Accrued Expenses mentioned on page 14, whatever expenses have been incurred that properly belong to the past period, such as wages due but unpaid, are liabilities; for the cash would be smaller by the amount of such postponed or accrued items had the claims been met during the period. The close relationship of both deferred charges and accrued expenses to cash is thus apparent—the one as an indirect addition to the cash, the other as an indirect deduction from or claim against cash. Accordingly, deferred charges are shown on the balance sheet immediately following the group of current assets, whereas accrued expenses are listed with the current liabilities as noted above.

The next group of assets is called Fixed Assets. Under this title are listed those assets which are used for carrying on the business but are not bought for the purpose of being resold. A certain amount of capital must be invested in the physical business plant. Furniture and fixtures, delivery equipment, buildings, land, machinery and tools, and so forth, must be purchased before the business can commence operating. It is assets of this type that comprise the class of fixed assets. [Pg 28] There is a corresponding group among the liabilities which are known as Fixed or Long-Term Liabilities. All debts maturing a year or more after the date of the balance sheet are classed as fixed liabilities. As examples of this class, we have long-term notes payable, mortgages payable, bonds payable, and so forth.

The difference between the fixed assets and the fixed liabilities indicates the amount of owner’s capital which has been invested in the business plant.

The final group of assets is called simply Other Assets, and includes all assets which cannot be classified in any other groups, such as good-will, patents, trade-marks, accounts and notes receivable having a credit term longer than six months, and other similar items. If there are any liabilities not capable of classification in the two groups of liabilities given above, they may be put in a group called Other Liabilities.

For the purpose of an easy showing of these various groups and their titles, it is customary to list the amounts of the several detailed items of each group in an inner money column, and to extend the total into the adjoining money column on the line of the last item in the group. A similar arrangement is made of the groups of liabilities so that not only the items in the various groups but the group totals as well are available. The totals of the various groups give the grand totals for the assets and the liabilities respectively.

The balance sheet as now classified and arranged provides first a formal title, giving the name of the business and the date of the balance sheet; then the assets, under which appear the groups Current Assets, Deferred Charges, Fixed Assets, and Other Assets; under the liabilities appear the groups Current Liabilities, Fixed Liabilities, and Other Liabilities. The showing of Proprietorship or Net Worth under the three different kinds of ownership has already been set forth. The illustration on page 31 shows a typical form of classified balance sheet. This should be studied carefully, as it is the type which will be used hereafter. [Pg 29]

The Problem of Content.—The form of the balance sheet serves the purpose of making easily available the information contained in the balance sheet. Form is of little value unless the content is accurate. What a balance sheet contains is, after all, far more important than its form. The problem of content comprises a consideration of two points: (1) the proper inclusion of all items, both assets and liabilities, belonging in the balance sheet; and (2) the correct valuation of the items so included.

With regard to the first, it may be said briefly that care must be exercised to see that all assets belonging to the business and having value, and that all claims against the business of whatever nature, are included.

Assuming that a given balance sheet contains a list of all the assets and all the liabilities, the further problem of the proper valuation of these items must be considered. A balance sheet in which the title Cash includes counterfeit bills, N. G. (that is, uncollectible) checks and other similar items, would not be considered a reliable balance sheet. Similarly, the basis for the valuation of each of the asset items must be investigated and determined correct before the balance sheet may be considered to represent the true financial condition of the business. It is the experience of every business that it cannot collect all of the credits extended to customers. Regardless of how carefully credit is granted, it will be found that some customers do not pay their debts. Accounts and notes receivable must, accordingly, be valued with a proper consideration for the estimated amount of the uncollectible portion. The stock of merchandise on hand must be valued according to the standard formula, at cost or market, whichever is the lower. The deferred charges group of assets will show the value of the unconsumed portions of the assets purchased, with due regard to the time element. Thus, a three-year insurance policy purchased at the beginning of the year will at the close of the year be valued at two-thirds of its original cost. The fixed asset group will be valued at cost less depreciation, which [Pg 30] represents the amount of the loss in value of the assets due to wear and tear, lapse of time, and obsolescence.

In determining liabilities, providing they have all been included, there is not the danger of an understatement, because their amount is subject to verification on the basis of the creditors’ claims. For obvious reasons the liabilities are seldom overstated.

General Principles Governing Form and Content.—In drawing up a balance sheet, the form must be flexible enough to meet whatever requirements for information may be placed upon it. Thus, a balance sheet to be presented to the banker as the basis of a loan should be carefully classified so as to show clearly the financial condition, and sufficient detail should be given to indicate the basis used in valuing the various items. A balance sheet drawn up for publication may, on the other hand, contain less detailed information and less attention need be given to its form. A balance sheet drawn up for use within the business itself may well contain very full information and its form should be such as will accurately portray the status of affairs. A balance sheet which shows on its face that cognizance is taken of uncollectible accounts and of the loss in fixed assets due to depreciation, is much more valuable as a financial statement than one lacking that information, provided of course it is to be used to indicate that consideration has been taken of those elements. Excepting for the general remark that regard must always be had to the purpose for which the balance sheet is drawn up, no hard-and-fast rule can be laid down in the matter of the relative fullness of detail with which it should be made.

Illustration. To illustrate the features of the balance sheet discussed in this chapter, the following statement showing the financial condition of the partnership of Jackson & Edwards is given: [Pg 31]

Jackson & Edwards

Balance Sheet June 30, 19—

| Assets | |||

| Current Assets: | |||

| Cash | $ 2,365.00 | ||

| Accounts Receivable | $8,500.00 | ||

| Less—Reserve for Doubtful Accounts | 170.00 | 8,330.00 | |

| Merchandise | 10,425.00 | $21,120.00 | |

| Deferred Charges: | |||

| License Fees Paid in Advance | $ 175.00 | ||

| Unexpired Insurance | 75.00 | ||

| Supplies | 80.00 | 330.00 | |

| Fixed Assets: | |||

| Furniture and Fixtures | $ 750.00 | ||

| Less—Reserve for Depreciation | 75.00 | $ 675.00 | |

| Buildings | $9,680.00 | ||

| Less—Reserve for Depreciation | 242.00 | 9,438.00 | |

| Land | 2,500.00 | 12,613.00 | |

| Total Assets | $34,063.00 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Notes Payable | $2,500.00 | ||

| Accounts Payable | 6,750.00 | ||

| Wages Accrued | 250.00 | ||

| Interest Accrued | 75.00 | $ 9,575.00 | |

| Fixed Liabilities: | |||

| Mortgage on Land and Buildings | 2,500.00 | ||

| Total Liabilities | 12,075.00 | ||

| Net Worth | |||

| Represented by: | |||

| S. J. Jackson, Capital | $10,267.00 | ||

| P. R. Edwards, Capital | 11,721.00 | $21,988.00 | |

[Pg 32]

Comparison of Net Worths.—The aim of every business enterprise is to increase its net worth. If James Runyon at the beginning of the year is worth $5,000 and at its close $7,500, it is evident that he has increased his wealth by $2,500. Very little information is given him or anyone else as to the manner in which the increase took place, except that it came about in the ordinary course of business. No criterion is given by which to compare effort with result. An increase of $2,500 may or may not be commensurate with the labor expended in effecting it. However, since a business is not likely to remain stationary, there is a degree of satisfaction in knowing merely the extent of the change in its net worth. The taking of an inventory, the appraising of the value of the assets from time to time, and the setting of the liabilities for the same dates over against them, is the method of determining the corresponding net worths. A comparison of these net worths shows their increase or decrease during the period. A further analysis of the individual items may be made. A comparison of each asset at the beginning of the period with its value at the end of the period, shows the increase or decrease in that item. A similar comparison of each liability item brings out the increase or decrease during the period.

How a Gain or Loss May Be Evidenced.—During a period a gain or increase in net worth may come about in one of four ways:

1. The assets may remain the same and the liabilities may decrease.

2. The liabilities may remain the same and the assets may increase.

3. The assets may decrease but the liabilities suffer a greater decrease.

4. The assets may increase but the liabilities undergo a smaller increase.

[Pg 33] Provided no more money has been invested in the business, and none has been withdrawn, there has been in all the above instances an increase in net worth, that is, a profit has resulted. If the reverse of the above relationships obtains, there has been a decrease in net worth, or a loss.

The following statements illustrate the points discussed above.

Aaron Conners

Balance Sheet,

June 30, 1921

| Assets | ||

| Cash | $ 1,000.00 | |

| Notes Receivable | 250.00 | |

| Accounts Receivable | 5,250.00 | |

| Merchandise | 8,500.00 | |

| Store Fixtures | 525.00 | |

| Total Assets | $ 15,525.00 | |

| Liabilities | ||

| Accounts Payable | $ 5,365.00 | |

| Notes Payable | 1,250.00 | |

| Total Liabilities | 6,615.00 | |

| Net Worth | ||

| Aaron Conners, Capital | $ 8,910.00 | |

One year later Conners’ financial

condition is shown to be:

Aaron Conners

Balance Sheet,

June 30, 1922

| Assets | ||

| Cash | $ 850.00 | |

| Notes Receivable | 100.00 | |

| Accounts Receivable | 6,425.00 | |

| Merchandise | 10,260.00 | |

| Store Fixtures | 472.50 | |

| Delivery Equipment | 350.00 | |

| Total Assets | $ 18,457.50 | |

| Liabilities [Pg 34] | ||

| Accounts Payable | $ 6,192.75 | |

| Notes Payable | 950.00 | |

| Accrued Salaries | 50.50 | |

| Total Liabilities | 7,193.25 | |

| Net Worth | ||

| Aaron Conners, Capital | $ 11,264.25 | |

The various types of information essential to judging the financial condition as disclosed by the above balance sheets will now be discussed.

Comparison of Balance Sheets.—A comparison of balance sheets gives more information than merely the amount of profit for the year. It indicates trends in the business. Thus a comparison of the notes and accounts receivable for the two years may give some indication of the vigor with which collections are pressed. If the volume of business done, that is, the amount of sales made, was about the same during the two years, and if there are more uncollected accounts at the close of the second year than at the close of the first, it would tend to show that collections were less satisfactory during the second year. Investigation may show that this is due to general conditions of business in the country rather than to failure to push collections vigorously. If there is any marked change in the amount of the stock of merchandise on hand it would invite inquiry. If the stock is much larger at the end of the second year than at the end of the first, it might indicate that the business man is speculating in merchandise, that he considers the buyer’s market during the year particularly favorable and has laid in an abnormally large stock. A banker with large experience in similar businesses can formulate a fairly accurate judgment of how much working capital a concern should have invested in merchandise. With that as a criterion he can tell the normal amount of merchandise the business should carry. [Pg 35]

A comparison of current liabilities for the two periods will indicate the extent to which borrowed working capital is being used. Thus, an unusual increase in stock-in-trade may be offset by an equally large increase in current liabilities, and so would indicate that the merchant has done his buying on credit or has used borrowed working capital to increase his stock. The danger of this is apparent in a fluctuating merchandise market, particularly if the swing is generally downward. A comparison of the working capital for the two periods gives useful information. A decrease in the amount of working capital may indicate an investment of it in fixed plant which, if continued, will lead to trouble with current creditors. An increase in working capital may point to the advisability of greater sales effort.

A comparison of fixed assets for the two periods will show the increase or decrease in the plant investment. If this has been offset by a corresponding increase or decrease in fixed liabilities, no additional capital of the owners has become tied up in fixed plant, while the reverse is true if there is not that correspondence between fixed assets and fixed liabilities. Where the ratio between current liabilities and fixed liabilities has increased, it may point to the desirability of funding some of the current debt. Short-term liabilities have apparently been incurred for the purpose of extending the fixed plant. It is usually desirable to convert, that is, fund these current liabilities into long-term liabilities in order to conserve working capital to pay current debts.

Thus it is seen that a proper understanding of the items in the two balance sheets and of their various interrelationships will oftentimes give very valuable information. Banks and business houses which are called upon to extend credit, maintain regular files of credit information, including periodic balance sheets, concerning their present and prospective customers, so that they can judge fairly accurately the condition of the businesses.

The Comparative Balance Sheet—Its Content and Form.—A [Pg 36] comparison of the above balance sheets shows an increase of net worth of $2,354.25 during the year. It shows also that this profit is accounted for by an increase of $2,932.50 in the assets, which is offset by an increase of $578.25 in the liabilities, leaving a net increase of $2,354.25.

The two statements thus separated do not lend themselves easily to a comparison of individual items. Accordingly, a method of showing the comparison known as the “Comparative Balance Sheet” form is used. This brings all the data into juxtaposition and so makes comparison easy. The balance sheet for the current year is shown first, followed by that for the preceding year. The increase and decrease column uses the current year as a basis for comparison with the preceding year.

Aaron Conners

Comparative Balance Sheet,

June 30, 1922 and June 30, 1921

| Assets | 1922 | 1921 | Increase and Decrease |

||

| Current Assets: | |||||

| Cash | $ 850.00 | $ 1,000.00 | - | $ 150.00 | |

| Notes Receivable | 100.00 | 250.00 | - | 150.00 | |

| Accounts Receivable | 6,425.00 | 5,250.00 | + | 1,175.00 | |

| Merchandise | 10,260.00 | 8,500.00 | + | 1,760.00 | |

| $17,635.00 | $15,000.00 | + | $ 2,635.00 | ||

| Fixed Assets: | |||||

| Store Fixtures | $ 472.50 | $ 525.00 | - | $ 52.50 | |

| Delivery Equipment | 350.00 | + | 350.00 | ||

| $ 822.50 | $ 525.00 | + | $ 297.50 | ||

| Total Assets | $18,457.50 | $15,525.00 | + | $2,932.50 | |

Liabilities |

|||||

| Current Liabilities: | |||||

| Accounts Payable | $ 6,192.75 | $ 5,365.00 | + | $ 827.75 | |

| Notes Payable | 950.00 | 1,250.00 | - | 300.00 | |

| Accrued Salaries | 50.50 | + | 50.50 | ||

| Total Liabilities | $ 7,193.25 | $ 6,615.00 | + | $ 578.25 | |

Net Worth |

|||||

| Aaron Conners, Capital | $ 11,264.25 | $ 8,910.00 | + | $2,354.25 | |

[Pg 37] While it is true that a great deal of valuable information can be secured from a comparative balance sheet, and that this form of balance sheet locates definitely the changes in the asset and liability items, summarizes those changes, and shows the net profit, it nevertheless fails to disclose the forces within the business organization which have brought about the changes—it sets forth effect or result but not cause. A supplementary or rather a complementary statement is needed to show the reasons for the changes. This is discussed in the following two chapters.

[Pg 38]

Fuller Information Needed.—As indicated in Chapter IV, in the summarization of the business transacted during a given period, it is not usually sufficient to know how much net worth has changed; nor is the whole story told when it is known exactly what items are responsible for the change, that is, which of the properties are worth more and which are worth less at the end than at the beginning of the period. Additional information is necessary to account for the changes shown by the comparative balance sheet.

The proprietor who knows simply that his cash is $1,000 less now than it was at the corresponding time in the last fiscal period, has not the kind of control over his business that his competitor has who knows that the $1,000 was expended for an increased stock of goods, or that an outstanding liability of that amount has been settled, or that his expenses for the period have been larger by $1,000 than for the former period. His competitor may be worse off but he at least has the advantage of knowing the reason for his being so. He has made a correct diagnosis of the pulse beat of his business. If he cannot heal its ills or secure aid for it, he can at least have the satisfaction of giving it a respectable burial, and the autopsy will then disclose that he failed to take advantage of his information until it was too late.

However, the point should be clearly held in mind that the proprietor who knows exactly what is happening in his business is in a position to exercise a definite and sure control over it. Hence, the accounting department, to justify its existence, should aim to give full [Pg 39] information as to what is taking place within the business and what eventually will be the result in its financial life. Only in this way can the department serve as a means of control.